Learn how to improve your credit score with proven strategies that work. Discover the fastest way to improve credit score, boost your credit score for free, and build better credit in 2026.

How to Improve Credit Score: Quick Answer

If you’re wondering how to improve credit score, start by paying every bill on time, lowering your credit card balances, checking your credit reports for errors, avoiding unnecessary credit applications, and keeping older credit accounts open. These habits have the biggest impact on your FICO Score and can help you see improvements in as little as 30 to 60 days. If you want the fastest way to improve credit score, focus on reducing your credit utilization and correcting any inaccurate information on your credit reports.

Introduction

Your credit score is much more than just a number. It plays a major role in your financial life, influencing whether you qualify for a mortgage, auto loan, credit card, apartment, or even certain employment opportunities. It can also determine how much you’ll pay in interest over the life of a loan.

Short Summary Table

| Credit Score Improvement Step | Quick Overview |

|---|---|

| Pay Every Bill on Time | Payment history is the biggest credit score factor. Even one late payment can hurt your score, while consistent on-time payments help build excellent credit. |

| Keep Credit Utilization Low | Aim to use less than 30% of your available credit, and ideally below 10% for the best results. |

| Review Your Credit Reports | Check your credit reports regularly for errors or fraudulent accounts and dispute inaccurate information as soon as possible. |

| Keep Older Credit Accounts Open | Older accounts strengthen your credit history and help lower your overall credit utilization ratio. |

| Limit New Credit Applications | Apply for new credit only when necessary to avoid multiple hard inquiries that can temporarily lower your score. |

| Build Positive Credit History | Use secured credit cards, credit-builder loans, or become an authorized user to establish a strong payment history. |

| Maintain a Healthy Credit Mix | Managing different types of credit responsibly can slightly improve your overall credit profile over time. |

| Monitor Your Credit Regularly | Track your credit score and review your reports frequently to identify issues early and monitor your progress. |

| Improve Credit Without Debt | If you have no debt, build credit by using a secured credit card responsibly or becoming an authorized user on a trusted account. |

| Boost Your Credit Score for Free | Correct reporting errors, pay on time, keep balances low, and use free credit monitoring tools to improve your score without spending money. |

| Avoid Common Credit Mistakes | Missing payments, maxing out credit cards, closing old accounts, and applying for too much credit can slow your progress. |

| How Long Does It Take? | Some improvements may appear within 30–60 days, while building an excellent credit score usually requires several months of consistent financial habits. |

The good news is that improving your credit score doesn’t require secret tricks or expensive services. Most people can make meaningful progress by developing a few smart financial habits and staying consistent.

Whether you’re trying to buy your first home, refinance existing debt, qualify for better credit cards, or simply strengthen your financial future, understanding how credit scores work is the first step.

This guide explains exactly what affects your score and the practical actions you can take to improve it.

How Credit Scores Work

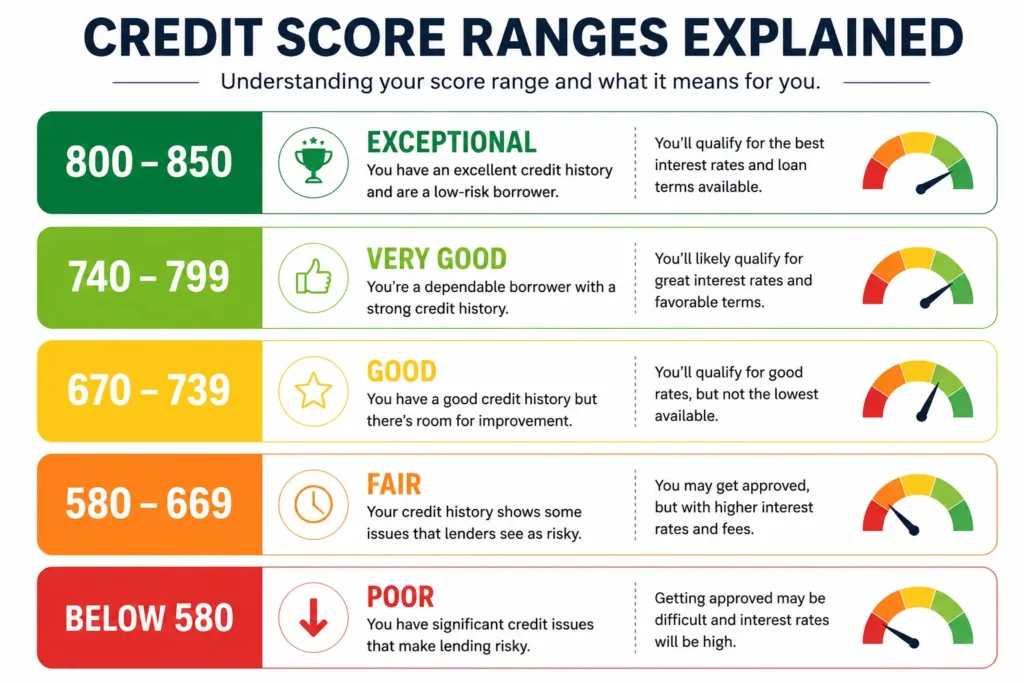

Most lenders in the United States use the FICO Score, although some also consider VantageScore. Both scoring models generally range from 300 to 850, with higher scores indicating lower lending risk.

Here’s a general breakdown:

- Exceptional: 800–850

- Very Good: 740–799

- Good: 670–739

- Fair: 580–669

- Poor: Below 580

While different lenders may use different scoring models, the habits that improve your score remain largely the same.

The Five Factors That Influence Your Credit Score

Understanding these factors helps you focus on the actions that deliver the biggest results.

Payment History (35%)

Your payment history carries the greatest weight. Paying every bill on time shows lenders you manage debt responsibly.

Credit Utilization (30%)

This measures how much of your available revolving credit you’re currently using. Lower utilization generally leads to higher scores.

Length of Credit History (15%)

Older accounts demonstrate long-term financial responsibility. Closing old accounts can sometimes reduce the average age of your credit history.

Credit Mix (10%)

Having different types of credit, such as credit cards, auto loans, and mortgages, can slightly improve your score when managed responsibly.

New Credit (10%)

Opening several new accounts within a short period may temporarily lower your score because of hard inquiries and reduced average account age.

1. Pay Every Bill on Time

Credit Impact

Payment history is the single biggest factor affecting your credit score. Even one payment that’s more than 30 days late can significantly lower your score and remain on your credit reports for up to seven years.

What You Can Do

Set up automatic payments for at least the minimum amount due. If autopay isn’t possible, use calendar reminders or banking alerts so you never miss a payment.

If you’re experiencing financial hardship, contact your lender before missing a payment. Many lenders offer hardship programs that may help protect your payment history.

How Long It Takes

Positive payment history builds over time. While one month of on-time payments won’t create dramatic changes, several months of consistent payments can steadily strengthen your score.

2. Lower Your Credit Card Balances

Credit Impact

After payment history, credit utilization has the largest influence on your score.

For example, if your total credit limit is $10,000 and your balances total $5,000, your utilization is 50%. That’s generally considered high.

Many financial experts recommend keeping utilization below 30%, while scores often improve the most when utilization stays below 10%.

What You Can Do

If possible:

- Pay more than the minimum payment.

- Make multiple payments throughout the month.

- Pay before your statement closing date.

- Avoid making large purchases if you’re planning to apply for new credit soon.

Reducing utilization is often the fastest way to improve credit score, especially if your balances are currently high.

How Long It Takes

Most credit card companies report balances once every month. As lower balances are reported, many people begin seeing improvements within one or two billing cycles.

3. Review Your Credit Reports for Errors

Credit Impact

Incorrect information can unfairly lower your score.

Common errors include:

- Accounts that don’t belong to you.

- Incorrect payment history.

- Duplicate accounts.

- Wrong account balances.

- Identity theft-related activity.

These mistakes can make lenders believe you’re a higher-risk borrower than you actually are.

What You Can Do

Review your credit reports carefully from all three major credit bureaus.

Look for information that seems inaccurate or unfamiliar. If you discover an error, submit a dispute with the reporting bureau and provide any supporting documentation.

Correcting inaccurate information is one of the easiest ways to boost credit score for free because it doesn’t require paying down debt.

How Long It Takes

Many disputes are resolved within 30 to 45 days. Once corrected, your credit score may improve relatively quickly depending on the type of error removed.

4. Keep Your Oldest Credit Accounts Open

Credit Impact

The age of your accounts matters.

Older accounts increase the average age of your credit history, which helps demonstrate long-term financial stability.

Closing an old credit card may also reduce your available credit, causing your utilization ratio to increase.

What You Can Do

Even if you rarely use your oldest credit card, consider keeping it active by making a small purchase every few months and paying the balance in full.

If the card charges an annual fee, ask your issuer whether you can switch to a no-annual-fee version while keeping the same account history.

How Long It Takes

Keeping older accounts open benefits your score gradually over many years. Closing them, however, can have a much faster negative impact if it significantly increases your utilization ratio.

5. Apply for New Credit Only When Necessary

Credit Impact

Each credit application may result in a hard inquiry, which can temporarily lower your score by a few points.

While one inquiry usually isn’t a major concern, multiple applications within a short period can signal financial stress to lenders.

What You Can Do

Before applying for a new credit card or loan:

- Check whether prequalification is available.

- Compare offers before submitting applications.

- Avoid opening several new accounts at once.

If you’re shopping for an auto loan or mortgage, complete your rate shopping within a short period since many scoring models treat multiple inquiries for the same type of loan as a single inquiry.

How Long It Takes

Hard inquiries typically affect your credit score for about one year, although they remain visible on your credit report for up to two years.

A Quick Tip for Faster Results

If your goal is how to improve credit score quickly, focus first on the factors that produce the fastest improvements:

- Reduce credit card balances.

- Correct reporting errors.

- Never miss a payment.

- Keep utilization below 10% whenever possible.

These strategies often produce noticeable improvements much sooner than actions like increasing the age of your credit history, which naturally takes time.

6. Build Positive Credit History With the Right Credit Tools

Credit Impact

If you have a limited credit history or are rebuilding after financial setbacks, adding positive payment history can gradually increase your score. While this factor doesn’t work overnight, it creates a stronger credit profile over time.

What You Can Do

Several financial tools can help you build credit responsibly:

Secured Credit Cards

A secured credit card requires a refundable security deposit, which usually becomes your credit limit. It’s an excellent option for beginners because your on-time payments are typically reported to the major credit bureaus.

Credit Builder Loans

Many banks and credit unions offer credit builder loans. Instead of receiving the money upfront, your payments are held in a savings account until the loan is paid off. Each on-time payment helps establish a positive credit history.

Become an Authorized User

If a trusted family member has an older credit card with a long history of on-time payments and low balances, becoming an authorized user may allow you to benefit from that positive account history.

How Long It Takes

Many people begin seeing improvements within two to six months, depending on their existing credit profile and how consistently they make payments.

7. Keep a Healthy Credit Mix

Credit Impact

Credit mix makes up about 10% of your FICO Score. While it isn’t the biggest factor, lenders like seeing that you can responsibly manage different types of credit.

Examples include:

- Credit cards

- Auto loans

- Personal loans

- Student loans

- Mortgages

What You Can Do

There’s no need to borrow money simply to improve your score. Instead, allow your credit mix to develop naturally as your financial needs change.

If you only have one credit card and are trying to establish credit, a secured card or credit builder loan may be a reasonable next step.

How Long It Takes

A stronger credit mix develops over several years, making it more of a long-term strategy than a quick fix.

8. Monitor Your Credit Regularly

Credit Impact

Monitoring your credit won’t directly increase your score, but it helps you identify problems before they become major issues.

Many people discover fraudulent accounts or reporting errors months after they occur. Catching them early can protect your credit.

What You Can Do

Check your credit reports regularly and review your credit score each month through your bank or a reputable credit monitoring service.

Pay attention to:

- New accounts you didn’t open

- Unexpected balance increases

- Missed payment reports

- Hard inquiries you don’t recognize

Monitoring your progress also keeps you motivated as your score improves.

How Long It Takes

Monitoring is an ongoing habit that protects your credit throughout your financial life.

How to Improve Credit Score if You Have No Debt

Many people assume they can’t build credit without borrowing money, but that’s not true.

If you have no debt and little or no credit history, focus on building positive activity rather than taking on unnecessary debt.

Here are some smart options:

- Open a secured credit card.

- Use the card for small monthly purchases.

- Pay the balance in full before the due date.

- Keep utilization below 10%.

- Consider a credit builder loan from a local credit union.

- Become an authorized user on a trusted family member’s account.

If you’re wondering how to improve credit score if you have no debt, the goal is to demonstrate responsible credit use, not to carry balances or pay unnecessary interest.

Boost Credit Score for Free

Not every credit improvement strategy costs money.

Here are several ways to boost credit score for free:

- Review your credit reports for errors.

- Dispute inaccurate information.

- Set up automatic payments.

- Keep old credit cards open.

- Pay your statement balance before the closing date.

- Ask for a credit limit increase if you qualify.

- Become an authorized user on a trusted account.

- Monitor your score regularly through free services.

Small changes can produce meaningful improvements without paying for expensive credit repair companies.

Common Mistakes That Can Hurt Your Credit Score

Avoiding these mistakes is just as important as following good habits.

Missing Payments

Even one late payment can significantly damage your score.

Maxing Out Credit Cards

Using most of your available credit increases your utilization ratio and may lower your score.

Applying for Too Much Credit

Submitting several applications within a short period can result in multiple hard inquiries.

Closing Old Credit Cards

Unless there’s a compelling reason, keeping older accounts open usually benefits your credit history.

Ignoring Your Credit Reports

Mistakes happen more often than many people realize. Reviewing your reports regularly allows you to catch problems before they grow.

Frequently Asked Questions

What is the fastest way to improve credit score?

The fastest way to improve credit score is usually lowering your credit card balances, reducing your credit utilization ratio, and correcting any inaccurate information on your credit reports. These changes may begin affecting your score within one or two billing cycles.

How long does it take to improve a credit score?

It depends on your credit profile. Lowering utilization may produce results within 30 to 60 days, while building a long history of on-time payments often takes several months or longer.

Does checking my own credit score hurt it?

No. Checking your own credit score creates a soft inquiry, which does not affect your credit score.

Should I carry a balance to build credit?

No. Paying your balance in full each month is generally the better strategy. You don’t need to pay interest to build a strong credit score.

Can I improve my credit score if I’ve had past financial problems?

Yes. While negative information may remain on your credit report for several years, consistent on-time payments and responsible credit use can gradually improve your score over time.

Final Thoughts

Learning how to improve credit score isn’t about finding shortcuts or secret tricks. It’s about building habits that show lenders you’re a responsible borrower.

Start with the actions that have the biggest impact. Pay every bill on time, reduce your credit card balances, keep your oldest accounts open, and monitor your credit reports regularly. If you’re looking for how to improve credit score quickly, focus first on lowering your credit utilization and correcting any reporting errors.

Remember that building excellent credit takes patience. Small improvements made consistently each month can lead to significant financial benefits in the future, including lower interest rates, better loan approvals, higher credit limits, and greater financial flexibility.

The sooner you start, the sooner you’ll begin building a stronger financial future.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.