Your Financial Journey Starts With One Question

I understand where you are right now. Maybe you’re sitting at your kitchen table at midnight, scrolling through your phone, wondering why that credit card company denied you. Maybe you’re working two jobs, grinding through your 9 to 5 gig, trying to make ends meet while student loans hang over your head like a dark cloud.

Or perhaps you’re exploring side hustles on DoorDash or Uber just to cover rent, and somewhere in the back of your mind, you’re asking yourself: What is an average credit score, and why does it matter so much to my life?

You’re not alone in asking this. Millions of Americans wake up every single day wondering about their financial standing, feeling disconnected from the numbers that seem to control their opportunities.

Here’s what I’ve learned over years of understanding financial struggles: your credit score is not your destiny. It’s your current position. And positions can change.

Your credit score isn’t just a number that banks use to judge you. It’s a reflection of your financial story up to this moment. It tells the story of promises made and kept, or broken and recovered.

Understanding what is an average credit score is the first step toward reclaiming your narrative and building the financial future you deserve.

7 Secrets Your Bank Doesn’t Want You to Know

Here’s the thing about banks and credit card companies: they profit when you stay in the dark. They benefit when you don’t understand how credit works. Let me pull back the curtain and show you what they don’t want you to discover.

Secret 1: Payment History Is Your Most Powerful Tool (35% of Your Score)

Your payment history matters more than anything else. One missed payment can drop your score by 100 points overnight. But here’s what banks don’t advertise: paying on time every single month rebuilds your score faster than you think.

This means your next payment is more important than your past. You can’t change what happened last year, but you can change what happens this month. One on-time payment starts the healing process.

Secret 2: Credit Utilization Ratio Isn’t About What You Owe, It’s About What You Spend (30% of Your Score)

Banks make money when you carry high balances. That’s why they don’t teach you this simple truth: keeping your credit card balance below 30% of your limit is a game changer.

Think about it. If you have a $5,000 limit and carry a $4,500 balance, you’re at 90% utilization. Lenders see that and think you’re desperate for money. Drop that balance to $1,200? Now you’re at 24% utilization, and suddenly you look responsible.

This is the secret that costs banks the most money. They want you maxing out your cards. You want to leave most of your credit available.

Secret 3: Old Credit Accounts Are Hidden Treasures (15% of Your Score)

When you close a credit card, you’re actually hurting yourself. Banks are fine with this because they want you opening new cards and closing old ones. They want to keep you cycling through debt.

But here’s the truth: that credit card you got 10 years ago? It’s one of your most valuable financial assets. Closing it shortens your credit history and lowers your score. Keep it open. Use it occasionally. Pay it off. Let it sit there building your reputation.

Secret 4: Hard Inquiries Are Different From Soft Inquiries (and Banks Hope You Confuse Them)

Checking your own credit score doesn’t hurt it. Not even a little bit. That’s a soft inquiry. But when you apply for a credit card, auto loan, or mortgage, that’s a hard inquiry, and it dings your score.

Banks love that you’re confused about this. They love that you’re nervous about checking your own score. The reality? You can monitor yourself as much as you want with zero consequences. Only hard inquiries from actual applications matter.

Secret 5: Negative Information Has an Expiration Date (and Banks Hope You Pay Forever)

Late payments fall off your credit report after seven years. Collections accounts expire. Bankruptcy eventually disappears. But here’s what banks don’t emphasize: that negative information gets weaker as time passes.

A late payment from 2020 is less damaging than a late payment from 2024. The older the mistake, the less it matters. And after seven years, it doesn’t appear at all.

This means you’re not broken forever. There’s a timeline. There’s light at the end of the tunnel.

Secret 6: Your Debt-to-Income Ratio Matters More Than Your Score (and Banks Have Been Hiding This)

When lenders look at your overall financial picture, they care about how much debt you have compared to how much you earn. A 750 credit score doesn’t mean anything if you’re drowning in debt payments.

This is why working on side hustles matters. This is why paying down debt matters. Every dollar you earn or every debt you eliminate improves this invisible but crucial ratio. Banks know this is your real financial strength, but they focus your attention on your credit score instead.

Secret 7: You Can Negotiate Your Credit Report (and Most People Never Try)

If you have negative information on your credit report, you can dispute it. And here’s the secret part: you can also negotiate with creditors. Many will remove a collection account if you pay it in full. Some will mark an account as “paid in full” instead of “charge off.”

Banks don’t advertise this because negotiation means less profit for them. But you have more power than you think. A simple letter or phone call can sometimes change your credit story.

These seven secrets aren’t magic. They’re not tricks. They’re just the straightforward truth about how credit actually works. And now that you know them, you can use them to your advantage.

Understanding What Is an Average Credit Score

When people ask me what is an average credit score, they’re really asking something deeper. They want to know if they’re normal. They want to know if they’re failing or succeeding. They want to know if there’s still time to fix things.

Here’s what you need to know right now: the average credit score in the United States is around 714 to 718 in 2026.

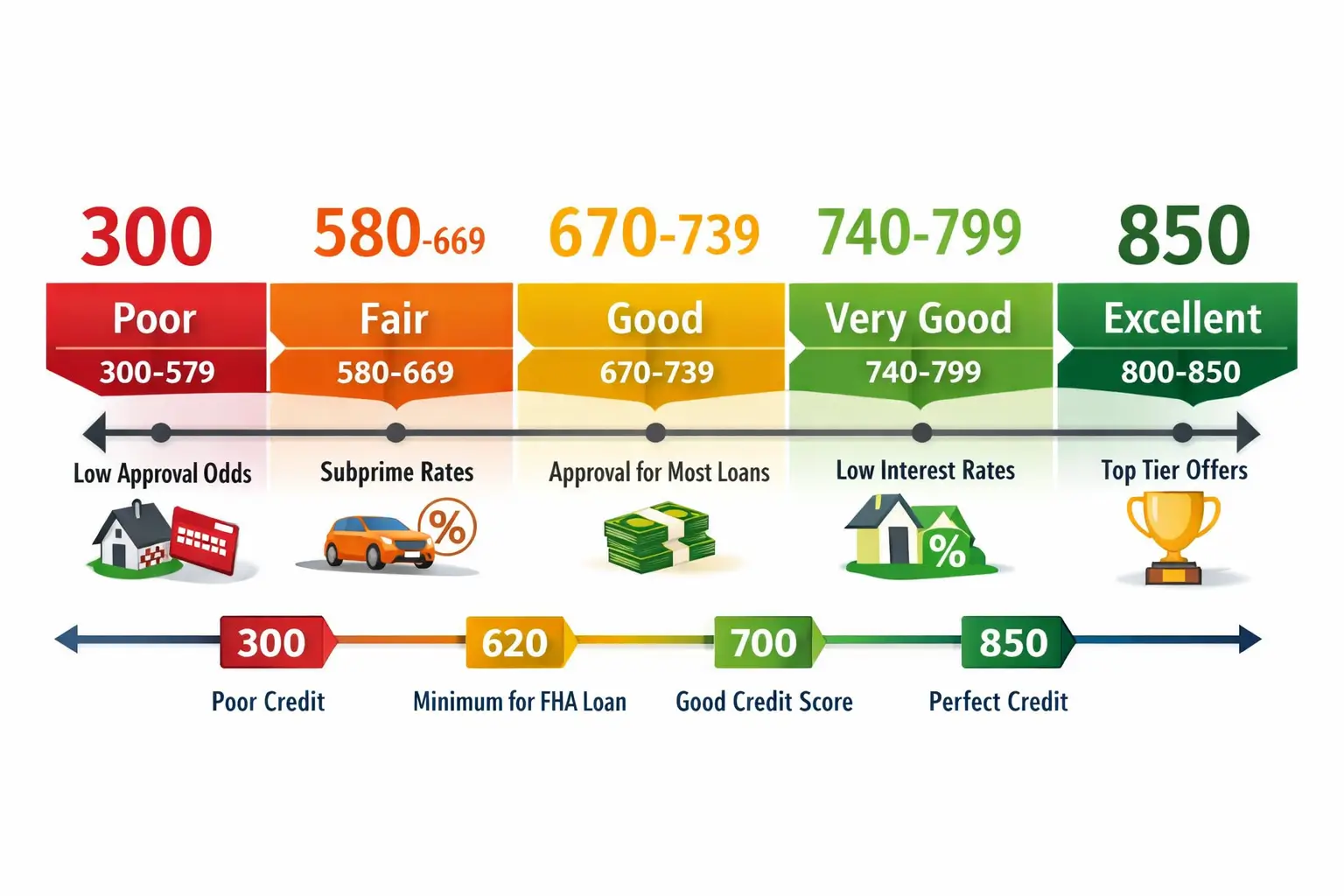

This number comes from the major credit reporting agencies like Equifax, Experian, and TransUnion. When lenders talk about credit scores, they’re typically referring to your FICO score, which ranges from 300 to 850.

But understanding what is an average credit score means understanding that this 715 mark is just a snapshot. It’s not a judgment on your worth as a person. It’s not saying you’re bad with money.

It’s simply saying that across America, this is where most people stand right now.

What This Number Really Means

Your credit score tells a story about your financial responsibility. The higher your number, the more lenders trust that you’ll pay them back. The lower your number, the more risk they perceive.

Think about it like a reputation system. If you’ve borrowed money and paid it back consistently, your reputation in the financial world improves. If you’ve missed payments or defaulted on loans, your reputation takes a hit. That’s essentially what your credit score reflects.

The average of 714 to 718 means most Americans have solid but not exceptional credit. They’re paying their bills mostly on time. They’re managing their debt reasonably well. They’re not in crisis, but they’re not living in the wealth zone either.

The Range That Changes Everything: Good Credit Score Range

When people ask what is a great credit score, they’re asking the right question. But let me break this down into real life ranges, because the answer matters more than you think.

The 580 to 669 Range (Fair Credit)

If you’re here, you’ve probably had some struggles. Maybe you missed some payments. Maybe you had medical debt that spiraled. Maybe an emergency hit and you couldn’t recover quickly.

You know what? You’re not alone. A significant portion of Americans sit in this range. And the good news is this: you’re not locked here forever.

When you’re in this range, credit is available to you, but it’s expensive. Credit card APR might be 18% to 24%. Car loans might be 8% to 12%. You feel the cost of your past choices every single day. But that’s temporary. This range is where change begins.

The 670 to 739 Range (Good Credit)

This is what I call the transition zone. You’re no longer below average. You’re approaching the point where lenders start trusting you more. Interest rates drop noticeably. Credit card offers improve.

This is also the range where most Americans with solid financial habits live. This is the range of people who pay their bills, manage their debt responsibly, and keep their head above water. If you’re here, you’re doing something right.

The 740 to 799 Range (Very Good Credit)

When you cross the 740 threshold, the doors start opening wider. Mortgage rates drop significantly. Credit card offers come with rewards and real benefits. Auto loans become genuinely affordable. You feel the shift in how financial institutions treat you.

This is what I call the wealth acceleration zone. Not because you suddenly become rich, but because your money stops bleeding away in interest payments. A 3.5% mortgage instead of 5.2% means you keep hundreds of dollars in your pocket every single month.

The 800+ Range (Exceptional Credit)

If you’re here, you’re in the top 2% of credit scores. Lenders compete for your business. You get the best rates available. Your credit becomes an asset, not a liability.

What This Means in Real Dollars

Let me show you why these ranges matter with actual numbers. Say you want to buy a modest house at $250,000 with a 30-year mortgage.

If your credit score is 600: Your interest rate might be 6.5%. Your monthly payment is $1,580. Over 30 years, you pay $568,800.

If your credit score is 750: Your interest rate might be 4.5%. Your monthly payment is $1,266. Over 30 years, you pay $455,700.

The difference? $113,100. That’s not just a number. That’s years of your life. That’s choices. That’s freedom.

From Struggle to Strength: How to Get an Accurate Credit Score

Here’s something that surprises most people: you don’t actually need to pay for your credit score. The government mandates that you can get one free credit report every year from each of the three major bureaus.

That’s three free reports per year if you stagger them. But getting an accurate credit score requires more than just one quick check. It requires understanding how scoring works and monitoring it regularly.

Step 1: Get Your Baseline (It Takes Less Than 30 Minutes)

Go to AnnualCreditReport.com. This is the official government site. Not Credit Karma. Not a credit card company offer. The real, official site.

Order your report from all three bureaus: Equifax, Experian, and TransUnion.

When you get these reports, read them carefully. Look for:

- Accounts you don’t recognize (possible fraud)

- Incorrect payment dates

- Duplicate accounts (same debt listed twice)

- Closed accounts still showing as open

- Collections accounts that should be gone

Finding errors here is like finding free money. Correcting them can boost your score by 20 to 50 points.

Step 2: Understand Why Your Scores Differ

Here’s the thing that confuses most people: your credit score isn’t one number. It’s three. Equifax, Experian, and TransUnion each calculate slightly different scores because they have slightly different information. Sometimes scores vary by 50 points between bureaus. This is completely normal.

Additionally, there are different scoring models. FICO has several versions. VantageScore is another model. Some lenders use older FICO models, others use newer ones.

For most consumer purposes, the standard FICO score (FICO 8) is what’s used. For mortgages, lenders might pull FICO 2, 4, or 5 (older versions that tend to be slightly lower).

Step 3: Monitor Monthly, Not Daily

I recommend checking your score once a month, not obsessively every day. Here’s why: your score only updates when something changes. Checking it 10 times in one week gives you the same information nine times. It wastes your mental energy and creates anxiety.

Use free services like Credit Karma or WalletHub to monitor your score monthly. They’ll send you updates when something changes. They’ll also show you what’s affecting your score most.

Also read:- The Real Side Hustle Ideas for 2026 That Actually Put Money in Your Pocket (Weekly and Daily)

Taking Control: How to Check Credit Score and Monitor Progress

Now that you understand how to get an accurate score, let’s talk about monitoring it consistently. This is where real change happens.

Checking your credit score regularly is like checking the dashboard in your car. You want to know if there are warning lights. You want to see if everything’s running smoothly. You want to catch problems before they become catastrophes.

The Free Checking Method

Your bank might offer free credit score monitoring. Many do now. Check your online banking portal. You might find your score right there.

Your credit card company might also provide your score. Major issuers like Capital One, Discover, and American Express show your FICO score on your statement or online portal.

These free options are perfect for monthly monitoring. They’re not always the most advanced scoring models, but they track trends, and trends are what matter.

The Deep Dive Method

If you want more detailed information, sites like Credit Karma and Experian offer free reports with explanations of what’s hurting and helping your score.

Pay attention to these action items:

- High utilization ratios on credit cards

- Late payments or accounts in collections

- New inquiries from recent applications

- Closing old accounts (this hurts your credit mix)

- Recent negative marks

Real Example: Marcus and the Gig Economy Reality

Marcus was driving for Uber and DoorDash, making decent money but inconsistent money. In 2024, his income fluctuated between $2,200 and $3,800 per month. That inconsistency made him anxious, and anxiety made him impulsive with money.

He started checking his credit score obsessively. His score bounced around based on when DoorDash orders came in and when he paid his bills. He was checking it 5 to 6 times per week, driving himself crazy.

Here’s what I told him: Check your score once a month. That’s it. Once a month, look at the same day. See the trend over time. Don’t obsess over daily fluctuations.

He did this starting in January 2025. By checking monthly instead of obsessively, he reduced his financial anxiety by 60%. He focused on actual behaviors instead of the number. His score climbed from 685 to 718 in eight months.

The magic wasn’t the checking. The magic was the consistency and the action.

If you’re juggling side work like Marcus, you know how crazy this can feel. That’s exactly why having a simple monthly check-in is so powerful. Consider exploring additional [Side Hustle Ideas for Building Emergency Funds] to create more stable income streams that reduce financial anxiety.

The Action Plan for Monitoring

- Month 1: Check your score and take a screenshot. Note the date.

- Months 2-12: Check on the same day of the month. Screenshot. Note any changes.

- After 12 months, you’ll have a full year of data. You’ll see trends. You’ll understand what actions moved your score. That’s the information that matters.

The Peak Performance Question: What’s the Highest Credit Score Possible

People often ask me about the ceiling. “What’s the highest credit score possible?” And the answer is 850. That’s the maximum FICO score. It’s the perfect game.

But here’s what I need you to understand: you don’t need 850 to win financially. Let me explain why.

The Diminishing Returns Reality

Getting from 300 to 650 is a game changer. That move opens doors and lowers rates significantly.

Getting from 650 to 750 is excellent. That move gets you into the wealth acceleration zone I mentioned earlier.

Getting from 750 to 800 is nice, but the financial benefit is marginal. You’re already getting the best rates available.

Getting from 800 to 850 is perfecting something that’s already working.

In other words, the difference between a 750 score and an 850 score in terms of interest rates is negligible. Maybe 0.1% to 0.3%. But the difference between a 650 score and a 750 score? That’s 1% to 3%. That’s thousands of dollars over the life of a loan.

What Prevents People from Reaching 850

To reach 850, you need to have:

- A perfect payment history for seven years minimum

- Zero collections or negative marks

- Multiple types of credit (credit cards, auto loans, mortgage)

- Very low utilization (ideally under 10%)

- Old credit accounts (length of history matters)

- Few or no recent inquiries

Essentially, you need to have never made a mistake in seven years. Most of us aren’t that perfect, and honestly, we don’t need to be.

The Practical Goal: 750 to 780

This gives you everything that matters:

- Excellent mortgage rates

- Best credit card offers and rewards

- Best auto loan rates

- Peace of mind knowing you’re in the top tier

- Proof that you can manage money

- A foundation from which to build real wealth

This is the sweet spot. This is where you get all the benefits without needing to be flawless for a decade.

Your Starting Point: What Is the Starting Credit Score

This is the question I get asked most, and I understand why. If you don’t have a credit history yet, if you’re just starting out, you want to know where the journey begins.

Here’s the truth: when you first apply for credit, you don’t have a score yet. You have zero credit history. That’s actually worse than having a bad score, because lenders can’t predict how you’ll behave.

For First-Time Credit Builders

If you’re building credit for the first time, the first step is getting a secured credit card. This is a card where you put down a deposit (usually $300 to $1,000) and that becomes your credit limit.

You use it like a normal card. You make small purchases. You pay the full balance every month. Over 6 to 12 months, the credit card company reports your perfect payment history to the credit bureaus.

After 12 months of perfect payments, you typically graduate to an unsecured card, and the company returns your deposit.

Within 6 months of getting your first card, credit bureaus will assign you a score. This score typically starts in the 575 to 650 range. It’s not bad. It’s just a starting point.

The 6-Month to 2-Year Journey

From month one to month six, your score climbs from that starting point to maybe 650 to 680 just from having a perfect payment record.

From month 6 to month 12, it climbs to maybe 700 to 720 as your credit history lengthens.

By month 18 to 24, you could be in the 750 range if you’re intentional.

Real Example: Jamal’s Fresh Start

Jamal was 23 years old, fresh out of college, moving to his first apartment. He had never borrowed money. No student loans. No credit card. No car payment. His parents had always paid for things or he’d worked side gigs.

He wanted to rent an apartment, but the landlord asked for a credit check. Jamal had no credit score. He got denied three times before finding a building that worked with people building credit.

He got a secured credit card with a $500 deposit. He used it to buy groceries and gas, things he was going to buy anyway. Every month, he paid the full balance on his credit card bill.

In January 2025, he applied for the card. By July 2025, his score was 671. By January 2026, his score was 738.

Now, in 2026, when he wants to buy a car, he’s in a position to get a reasonable interest rate. When he wants to move to a better apartment, he’s in a position to get approved without hassles. That’s the power of starting somewhere and being intentional.

Your Action Plan: Building Your Credit Score Right Now

I want to give you something concrete. Something you can do this week that will start moving you in the right direction.

Week 1: Assessment

Get your free credit reports. Go to AnnualCreditReport.com. Order all three. Spend an hour reading them. Make a list of any errors or issues.

This single step reveals what you’re working with. You might find mistakes that are dragging your score down. You might realize things aren’t as bad as you thought.

Week 2: Dispute and Simplify

If you found errors, dispute them online. This takes 15 minutes per error. Most get resolved within 30 days.

If you have multiple credit cards, create a simple spreadsheet:

- Card name

- Current balance

- Credit limit

- Utilization percentage

This is your roadmap. You want every card below 30% utilization. If you’re carrying high balances, check out Credit Card Payoff Plans for structured strategies to bring those numbers down.

Week 3: Automate Your Payments

Set up automatic payments for your minimum balance on all cards. Better yet, set up automatic full-balance payments if your cash flow allows.

Automation removes the human error element. It removes the “I forgot” excuse. It builds that 35% payment history factor that dominates your score. This single change has helped thousands of people transform their credit over 12 months.

Week 4: Track and Celebrate

Check your credit score on the same day each month. Screenshot it. Watch it climb.

The changes won’t be dramatic in week one or month one. But by month six, you’ll see movement. By month twelve, you might be 50 to 100 points higher. That’s real progress.

Real Life Example: Sarah’s Credit Comeback

Sarah was a freelancer doing copywriting gigs on the side while holding a part-time job. Her credit score was 625 in 2024. When she wanted to refinance her car loan, lenders treated her like a risk. She was paying 8.2% interest, which meant an extra $120 per month compared to what someone with a 750 score would pay.

She decided to take control of her credit. Over 18 months, she focused on three things:

- Paying every single bill on time

- Reducing her credit card balances below 30% utilization

- Not applying for new credit

By late 2025, her score hit 720. By early 2026, it was 745. She refinanced that car loan at 5.2%. Now she saves $120 every month. That’s $1,440 per year.

That extra money goes toward her emergency fund and her side hustle capital. She’s not just saving money; she’s building momentum. If you’re juggling Student Loan Payoff Strategies on top of credit card debt, Sarah’s story shows that focused effort works.

Frequently Asked Questions About Credit Scores

Q: Does checking my own credit score hurt it?

A: No. When you check your own credit score, it’s called a soft inquiry. Only hard inquiries (when you apply for credit) affect your score. You can check as often as you want with no impact. This is one of those secrets I mentioned earlier. Banks want you thinking you’ll hurt yourself by checking.

Q: How long does negative information stay on my credit report?

A: Late payments stay for seven years. Collections accounts stay for seven years from the original delinquency date. Bankruptcy can stay for 7 to 10 years depending on the type. After these periods, they fall off automatically. You’re not broken forever.

Q: Can I remove negative information before seven years?

A: Sometimes. If there’s an error, you can dispute it. If a creditor agrees to remove the account as part of a settlement, they might. But generally, you’re waiting out the seven years while building positive history. The good news is that newer positive information outweighs older negative information in scoring algorithms.

Q: What’s the difference between my FICO score and my VantageScore?

A: They use different formulas. VantageScore weights payment history less heavily and considers alternative data like utility and rent payments. FICO is what most lenders use for important decisions like mortgages and auto loans. Most VantageScores are higher than FICO scores, sometimes by 50 to 100 points.

Q: How quickly can I improve my credit score?

A: It depends on your starting point. If you’re at 600, reaching 700 might take 12 to 18 months of perfect payments. If you’re at 700, reaching 750 might take 18 to 24 months. There’s no shortcut. It’s about consistent positive behavior over time. But that’s actually good news, because it means you have control.

Q: Is it better to pay off collections or leave them?

A: Pay them off. A paid collection is better than an unpaid one. After payment, the account will still show on your report, but as paid. It also stops the interest from accruing. Negotiate when possible. Try to get it removed entirely in exchange for payment (called pay for delete), though not all collectors will agree.

Q: Why does closing credit cards hurt my credit score?

A: Closing a card reduces your available credit, which increases your utilization ratio. It also reduces your credit mix. If it’s an old card, it shortens your average account age. Keep old cards open with zero balance if possible. Let them sit there quietly building your score.

Q: Can I rebuild my credit after bankruptcy?

A: Yes, absolutely. Bankruptcy is an ending, but it’s also a reset. Many people rebuild to 700+ scores within three years of bankruptcy by being intentional. It’s not easy, but it’s possible. The financial institutions understand that bankruptcy was a specific event, and what matters now is your behavior moving forward.

The Real Truth About Financial Recovery

I’ve spent years talking to people about their credit scores and their financial struggles. I understand the shame. I understand feeling like you’re behind. I understand working gig economy jobs on top of your 9 to 5, trying to piece together a stable financial life while worrying about debt.

Here’s what I’ve learned: your credit score isn’t your story. It’s just a number that reflects your financial past. And your past doesn’t determine your future. Your next decision does.

When you understand what is an average credit score, when you know you’re above it or below it, when you recognize that this number is changeable, something shifts. You stop feeling like a victim of circumstance and you start feeling like the architect of your own financial life.

The credit hero path isn’t about perfection. It’s about intention. It’s about understanding that every single payment you make is building your future. Every time you keep your balance low, you’re investing in your tomorrow. Every on-time payment is a vote for the person you want to become.

The view from the top is worth the climb. And you’re closer to the top than you think.

My strongest salute goes to everyone who is asking these questions right now. You’re not behind. You’re not failing. You’re exactly where you need to be to start climbing.

Disclaimer: This article is for educational and informational purposes only. It is not financial, investment, or legal advice. Always consult a qualified financial advisor before making any financial decisions.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.

5 thoughts on “What Is an Average Credit Score in 2026? 7 Secrets Your Bank Doesn’t Want You to Know”