I get it. You check your phone after a long day at your entry-level job or after finishing a string of DoorDash deliveries, and that sinking feeling hits when you see the credit card balance, the student loan payment due, and the rent that keeps climbing. You’re not alone in this. Millions of young Americans between 22 and 35 are carrying average student loan debt around $39,000 to $43,000 while dealing with credit card rates that often sit between 20% and 25% APR. Rent in many cities still averages over $1,600 for a one-bedroom, and inflation makes everything feel tighter.

You’re working hard, maybe juggling a 9-to-5 with gig work like Uber, Instacart, or freelancing, yet the progress feels slow. I’ve been there too with clients who felt overwhelmed. The good news? Small, consistent changes using these top 10 brilliant money saving tips can start easing that stress this year. These aren’t quick fixes. They’re practical, realistic steps tailored for young adults in the US that focus on both cutting costs and building habits that last.

Let’s walk through this together, one tip at a time. You’ll find clear actions, realistic dollar examples, and ways to handle the common challenges we all face in 2026.

Why These Saving Money Tips Matter Right Now for Young Adults

In 2026, with high-yield savings accounts still offering around 4% to 5% APY from banks like Varo or Vio Bank, but credit card debt costing you 20-25% in interest, every dollar counts more than ever. Many young adults are balancing student loans, rising rent, and irregular gig income while trying to build an emergency fund.

These financial tips for young adults combine clever ways to save money with honest strategies for debt and income. The goal isn’t perfection. It’s gaining a little control so you can sleep better and feel less stressed. You’ve got this, and small steps really do add up.

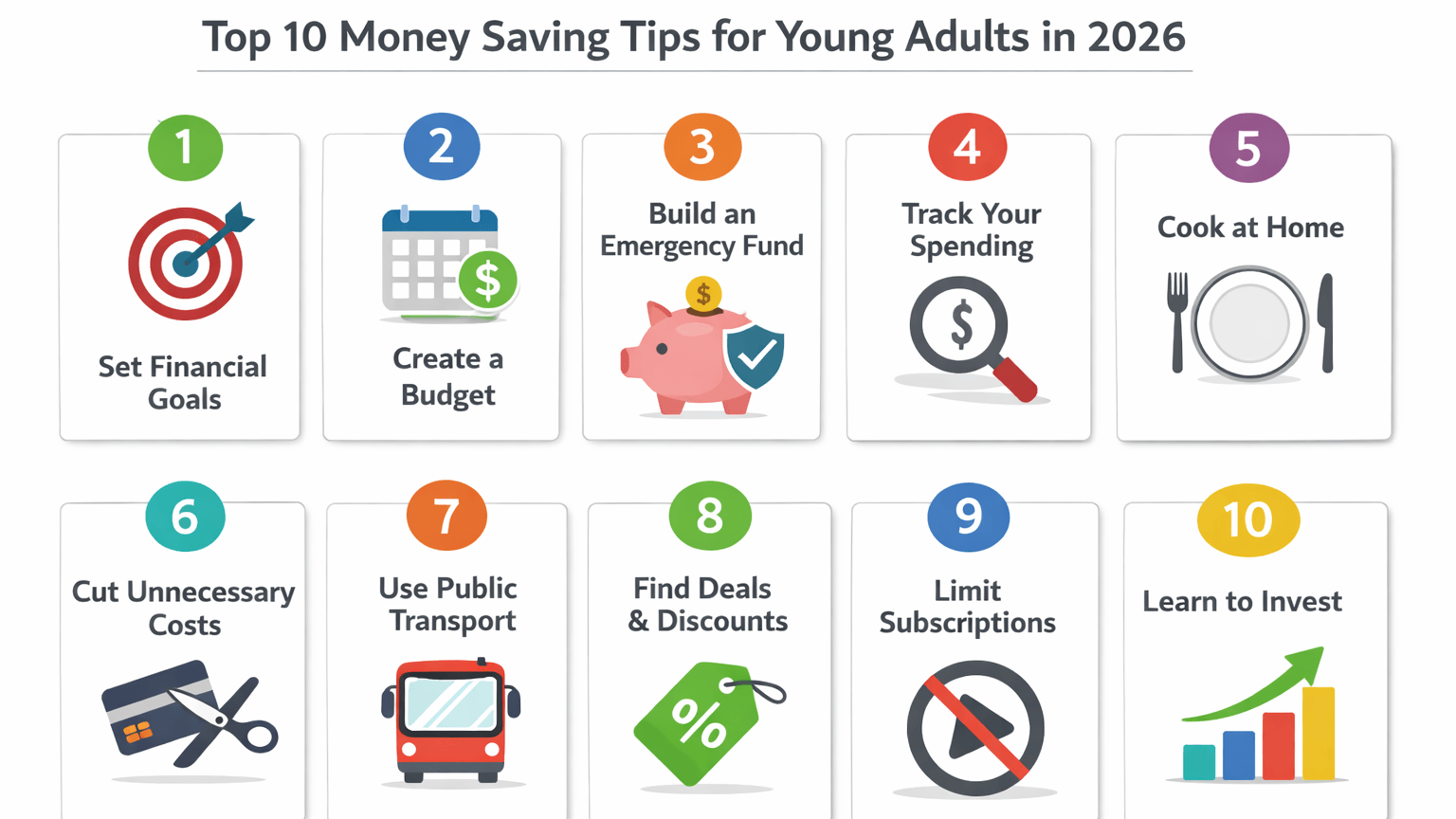

Tip 1: Track Your Spending Without Feeling Overwhelmed

Most people underestimate how much they spend on small things. Start simple. For one week, note every expense in your phone notes app or a free tool like Mint or your bank’s app. Include the $5 daily coffee, the $12 DoorDash order after a late shift, and subscription charges you forgot.

Actionable steps:

- Review last month’s bank and credit card statements.

- Categorize into needs, wants, and debt payments.

- Look for patterns without judging yourself.

One client discovered she was spending $180 a month on food delivery apps. Cutting back to twice a week saved her about $120 monthly. Common challenge? Feeling ashamed when you see the numbers. Overcome it by remembering this is information, not criticism. In 2026, many banking apps make tracking automatic and private.

This awareness is the foundation for all good saving money tips.

Tip 2: Create a Budget That Actually Works for Your Real Life

Forget strict budgets that feel impossible. Try the 50/30/20 rule as a starting point: 50% on needs (rent, utilities, minimum loan payments), 30% on wants, and 20% toward savings and extra debt payoff. Adjust it if your rent in a big city like New York or Los Angeles eats up 55-60%.

Actionable steps:

- List your take-home pay (after taxes).

- Subtract fixed costs like $1,600 rent or $300 student loan minimum.

- Allocate the rest intentionally.

For someone bringing home $3,800 monthly after an entry-level salary plus weekend gigs, that could mean $760 automatically going to savings and debt. A common challenge is irregular gig income. Solution: Base your budget on your lowest recent month and treat extra earnings as bonuses for debt or savings.

This approach has helped many young adults stop the paycheck-to-paycheck cycle.

Tip 3: Automate Savings So You Pay Yourself First

Automation removes the daily willpower struggle. Right after payday, set up an automatic transfer of even $50-$100 to a separate high-yield savings account.

Actionable steps:

- Open a high-yield savings account (current top rates around 4-5% APY with places like Varo offering up to 5% on qualifying balances).

- Set the transfer for the day after your direct deposit hits.

- Start small and increase as you get comfortable.

At 4% APY, $100 saved monthly grows faster than in a regular account paying almost nothing. One challenge is the temptation to dip into it. Keep this account at a different bank so it’s not too easy to access. In 2026, apps make this seamless.

You’re essentially paying your future self first, and that feels empowering.

Tip 4: Focus on High-Interest Debt First

Credit cards with 20-25% APR are expensive. Prioritize them using the debt avalanche method: Pay minimums on everything, then put extra money toward the highest interest balance.

Actionable steps:

- List all debts with balances and APRs.

- Make extra payments on the most expensive one.

- Consider balance transfer cards if your credit allows a 0% intro period (watch fees).

A young adult with $8,000 on a 24% card could save hundreds in interest by adding $150 extra monthly from gig work. Challenge: Feeling discouraged by the total balance. Overcome it by tracking the interest you’re avoiding each month. Many clients combine this with side income from Instacart or freelancing.

Tip 5: Reduce Everyday Expenses Without Feeling Deprived

Look at leaks like eating out, unused subscriptions, and impulse buys. Meal prep on Sundays to cut grocery and delivery costs by $150-200 a month.

Actionable steps:

- Review subscriptions and cancel two you rarely use (average savings $20-40 monthly).

- Bring coffee or lunch from home most days.

- Use cash or debit for discretionary spending to feel it more.

Challenge: Social pressure or stress eating. Solution: Plan affordable alternatives, like hosting friends for a potluck instead of going out. These clever ways to save money respect your need for enjoyment while freeing up cash.

Tip 6: Lower Your Biggest Costs – Housing and Transportation

Rent and cars often take the biggest bites. Consider a roommate to split a $1,800 two-bedroom, or negotiate your lease renewal.

For transportation, use public transit or bike for short trips if possible. Maintain your car to avoid big repair bills, or drive for Uber only when it truly adds net income after gas and wear.

Actionable steps:

- Shop around for insurance quotes annually (can save $200-400 a year).

- Explore slightly more affordable neighborhoods with good transit.

One client in a mid-sized city saved $300 monthly by adding a roommate and switching to biking two days a week. Common challenge: Fear of change. Start with one small adjustment and see how it feels.

(Image suggestion: Infographic comparing monthly costs before and after small housing/transport changes. Alt text: “Comparison chart showing potential monthly savings on rent and transportation for young adults.”)

Tip 7: Use Side Hustles to Fuel Your Savings and Debt Payoff

Gig work like Uber, DoorDash, or Instacart can help, but treat the income wisely. Decide upfront that 40-50% goes to debt or savings.

Actionable steps:

- Track your net earnings after expenses.

- Automate transfers from your gig account.

- Set boundaries to avoid burnout.

A freelance graphic designer I coached added $600 monthly from evening projects and directed half to her student loans. She paid off $4,200 in one year while still enjoying her main job. Challenge: Irregular income. Budget conservatively and build a buffer.

Tip 8: Make Your Money Grow in the Right Accounts

Once you have a small emergency fund (aim for $1,000 first, then 3 months of expenses), put it in a high-yield savings account earning 4-5% APY.

Consider contributing to a 401(k) if your employer matches, or open a Roth IRA for tax-free growth later.

Actionable steps:

- Research FDIC-insured options with no fees.

- Automate small contributions.

- Start with what you can, even $25 bi-weekly.

In 2026, that extra interest can add up to $200-300 a year on a growing balance without extra effort.

Tip 9: Shop and Spend More Intentionally

Before buying anything non-essential, wait 24-48 hours. Shop with a list and compare prices.

Buy generic where quality is similar, and wait for sales on bigger needs.

Actionable steps:

- Unsubscribe from marketing emails.

- Use browser extensions for coupons if you shop online.

- Ask: “Does this serve my goals?”

Clients often save $100+ monthly just by pausing impulse buys during stressful weeks.

Tip 10: Celebrate Progress and Build Lasting Momentum

Track wins monthly. Paid an extra $200 on debt? Added $150 to savings? Acknowledge it.

Treat yourself to something small and free or low-cost, like a home movie night.

Actionable steps:

- Keep a simple progress journal.

- Review every 30 days and adjust.

- Share with a supportive friend if it helps.

Momentum grows when you notice improvement. In 2026, that consistency can turn into real peace.

Real Stories From Young Adults Who Made It Work

Sarah, a 28-year-old teacher in Texas, was carrying $28,000 in student loans and $6,500 in credit card debt while renting a one-bedroom for $1,450. She felt exhausted from her 9-to-5 plus weekend tutoring. She started tracking spending, automated $100 monthly to a high-yield savings account, and used the avalanche method on her credit card. Within 18 months, she paid off the card completely, built a $4,000 emergency fund, and reduced her stress so much she could focus on enjoying her students again. “It wasn’t fast,” she told me, “but I finally felt in control.”

Marcus, 31, worked a warehouse job in Ohio making about $3,200 monthly after taxes and drove for Uber evenings. With $12,000 in credit card debt at 23% interest and rent taking a big chunk, he felt trapped. He created a simple 55/25/20 budget, cut food delivery, and directed 50% of his gig earnings to debt. He also switched to a high-yield savings account. After a year, he had paid down $7,800 of debt and saved $3,200. The emotional shift was huge. “I stopped dreading opening my banking app,” he shared.

These stories aren’t about being perfect. They’re about real young adults taking one step at a time.

FAQs

How much should I try to save each month as a young adult?

Start with whatever feels doable, even $50-100. As you cut expenses or add gig income, increase it. Consistency matters more than the amount at first.

Are high-yield savings accounts still worth it in 2026?

Yes. Top options offer 4-5% APY, which is significantly better than traditional accounts. Look for FDIC-insured banks with low or no fees.

What’s the smartest way to handle student loans while trying to save?

Make at least the minimum payments. Build a small emergency fund first so you’re not forced to add more debt during surprises. Then apply extra toward loans when possible.

Can side hustles really help without burning me out?

They can, if you choose flexible ones and set clear limits. Direct a portion of earnings straight to savings or debt so the work feels purposeful.

How do I stop impulse spending when I’m stressed from work or gigs?

Use the 24-hour rule and remind yourself of your “why,” like reducing debt stress. Replace the habit with something free, like a walk or calling a friend.

Is it possible to save while living paycheck to paycheck?

Yes. Many start with tiny automated transfers and one or two expense cuts. Progress builds gradually, and even $25 a week adds up.

What if I’ve tried budgeting before and it didn’t stick?

That’s common. Try a simpler version this time and be kind to yourself. Adjust as life changes. The right system supports you, not restricts you.

How do these tips specifically help with credit card debt?

By tracking spending, automating savings, and directing extra income from gigs or cuts toward the highest-rate card, you reduce the balance faster and avoid more interest.

You’ve made it this far, and that says a lot about your desire for change. These top 10 brilliant money saving tips and financial tips for young adults are here to support you where you are right now. Pick just one or two that feel doable this week. Maybe it’s opening that high-yield savings account or tracking spending for a few days.

You’re not alone in this journey. With steady steps, you can ease the debt weight, build a buffer, and create more space for the life you want. You’ve already got the strength. Take that first small action today. I’m rooting for you.

Disclaimer: This article is for educational and informational purposes only. It is not financial, investment, or legal advice. Always consult a qualified financial advisor before making any financial decisions.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.