Debt Snowball Method 2026: You wake up in the middle of the night again, heart racing, thinking about that credit card balance that never seems to go down no matter how much you pay. The student loans from years ago still sit there, growing quietly. Rent in your city keeps climbing, your 9 to 5 job barely covers the basics, and some months you wonder how you’re going to keep the lights on. I understand how it feels. That heavy weight in your chest when you open your banking app. The quiet shame when friends talk about vacations or buying a house while you’re just trying to stay afloat.

You’re not alone in this. Millions of people across the United States are carrying massive credit card debt, student loans averaging over forty thousand dollars, and the constant pressure of making ends meet in 2026. But here’s what I want you to hear right now: there is a way out that doesn’t require being perfect with money or having some high paying side hustle from day one. It’s called the debt snowball method, and it has helped so many regular people like you and me finally see progress when everything else felt impossible.

The debt snowball method works by focusing on your smallest debts first. You list out everything you owe from the smallest balance to the largest, keep making minimum payments on the bigger ones, and throw every extra dollar you can find at that smallest one until it’s gone. Then you take what you were paying on that first debt and roll it into the next smallest. It builds like a snowball rolling downhill, getting bigger and stronger with each win.

This isn’t about the math being perfect. It’s about how it feels to finally cross something off your list and breathe a little easier. In a year when living costs are still high and gig work like DoorDash or Uber feels like the only way to scrape together extra cash, this approach meets you where you are emotionally. It gives you those small victories that keep you going when motivation is low.

Why Debt Feels So Heavy Right Now

I have seen people go through this exact season. You’re working your regular job, maybe picking up evening deliveries or freelancing on weekends, and still the balances barely move because interest keeps piling on. Credit cards with rates over twenty percent make every payment feel like it’s barely denting the principal. Student loans sit in the background, and rent pressure means there’s never much left at the end of the month.

You might be feeling stuck right now, scrolling through articles late at night wondering if you’ll ever get ahead. That feeling is real, and it’s exhausting. But the debt snowball method acknowledges something important: paying off debt isn’t just a numbers game. It’s a feelings game too. When you knock out that first small balance, something shifts inside you. You start believing it’s possible.

In 2025 and into 2026, with economic pressures still lingering, many folks are turning to this method because it delivers quick emotional relief. You see progress fast, and that momentum helps you stick with it longer than strict math focused plans sometimes do.

How the Debt Snowball Method Actually Works Step by Step

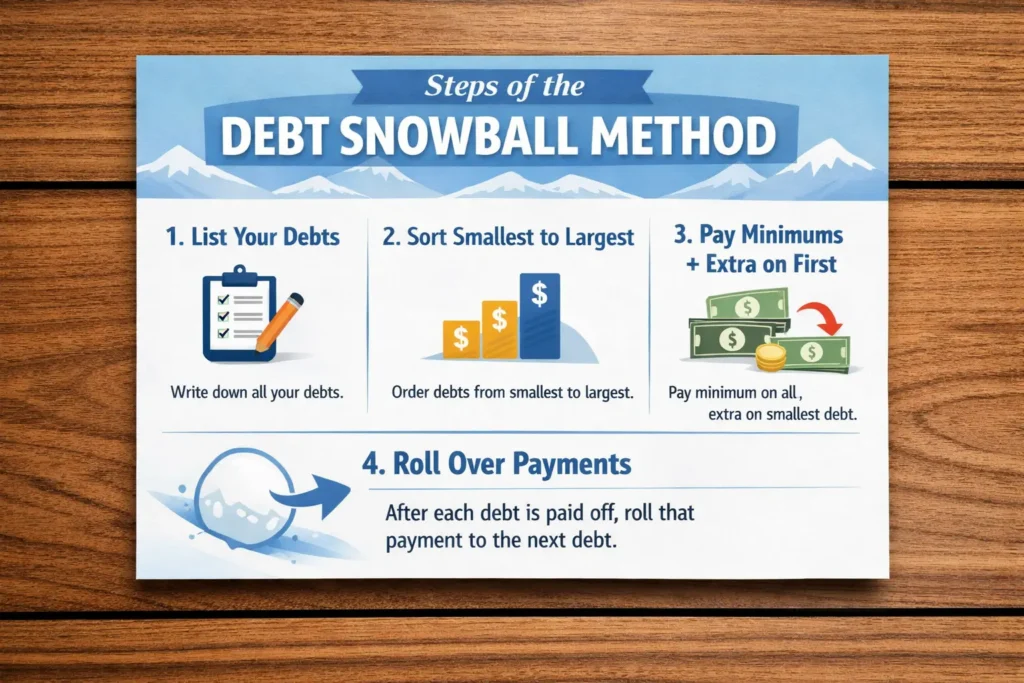

Let’s walk through this together like we’re sitting at your kitchen table with a cup of coffee. First, you gather every debt you have. Credit cards, personal loans, student loans, car payments, medical bills, whatever it is. Write them down with their current balances. Don’t worry about interest rates yet. Just the balances.

Sort them from smallest to largest. That tiny store card with four hundred dollars left? That’s your starting point. Make the minimum payments on everything else to keep them from falling behind. Then, find every extra dollar you can, maybe from cutting one subscription, skipping eating out a few times, or adding a couple of DoorDash shifts, and send it all to that smallest debt.

Once it’s paid off, celebrate quietly. Feel that win. Then add the full amount you were paying on it to the next smallest debt. Your payment on the second one grows. Keep going. The snowball gets bigger, and so does your confidence.

This method is practical for real life. If you’re in a city where rent takes half your paycheck, you don’t need to find thousands extra right away. Start with what you have, even if it’s fifty dollars a month beyond the minimums. Small consistent action compounds.

The Emotional Side No One Talks About Enough

I understand how it feels when debt makes you question your worth. You see others posting about their debt free journeys and think, “That could never be me.” But I’ve watched people who felt exactly like that start with one small card and slowly change their entire financial picture.

One woman I know in the Midwest had about eight thousand dollars spread across three credit cards from unexpected medical bills and everyday overspending during tough years. She was working a 9 to 5 and driving for Uber on weekends. Using the debt snowball, she targeted her smallest card first, about twelve hundred dollars. She cut her grocery spending a bit, added a few extra driving hours, and paid it off in three months. That first zero balance gave her such a boost that she kept going and cleared the rest within a year and a half.

It wasn’t perfect. There were months when life happened, a car repair or higher rent. But those small wins kept her from quitting.

Another example is a couple in Texas with over fifty thousand in student loans and credit cards after starting a family. They listed everything, started with a small personal loan, and used extra income from freelancing graphic design online. Each paid off debt gave them hope, and they eventually became debt free while still enjoying simple family time.

These aren’t fairy tale stories. They’re regular people facing the same pressures you are in 2026, with gig economy work, rising costs, and the daily grind.

Debt Snowball vs Avalanche: Which One Feels Right for Your Life

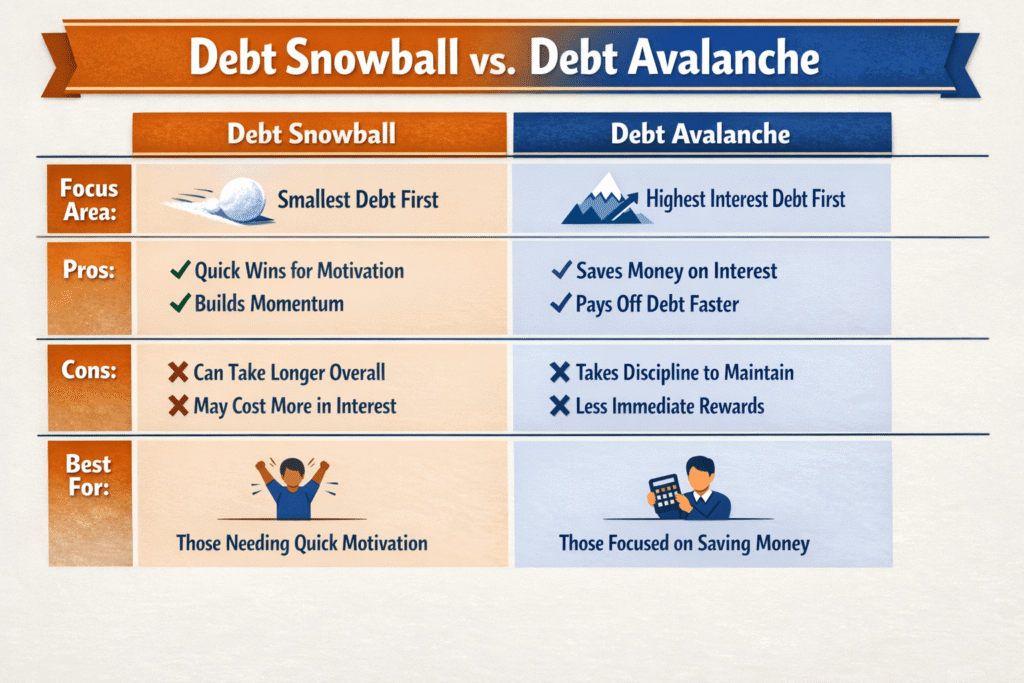

Now, you might hear about the debt avalanche method too. That’s where you focus on the highest interest rate debt first to save the most money on interest over time. It’s smart mathematically. If you have a credit card at twenty two percent and a student loan at six percent, the avalanche attacks the expensive one aggressively.

But here’s the honest truth many people discover: the avalanche can feel slow and discouraging if your highest interest debt is also one of the largest. You might go months without seeing a balance disappear completely, and that can wear you down when you’re already emotionally drained.

Debt snowball vs avalanche comes down to your personality and what keeps you moving forward. If you’re the type who needs visible progress to stay motivated, the snowball often wins in real life. Many folks pay a little more in interest but finish the journey because they didn’t burn out halfway.

Some people even do a hybrid. Start with snowball for the first couple of small debts to build momentum, then switch to avalanche for the bigger high interest ones. The key is choosing something you can actually stick with.

What is really stopping you right now from starting? Is it the fear that it won’t work, or just not knowing where to begin?

Making Extra Money to Fuel Your Snowball

The debt snowball works better when you add more to those payments. In 2026, the gig economy is still a lifeline for many. Driving for Uber or delivering with DoorDash a few evenings a week can bring in a few hundred extra dollars that go straight to your smallest debt.

Freelancing is another path. If you have skills in writing, graphic design, virtual assistance, or even social media management, platforms make it easier than ever to pick up side work. Start small. Even one extra client a month can make a difference.

But don’t burn yourself out. The goal is sustainable progress. Maybe you look at your current 9 to 5 and ask for a small raise, or cut one expense you won’t miss. Every little bit rolled into the snowball makes it grow faster.

Have you ever felt this pressure where every extra dollar seems to disappear before you can use it for debt? Many of us have. The snowball helps because it gives purpose to those hard earned extras.

Real Life Challenges and How to Handle Them

Life doesn’t pause just because you’re paying off debt. A medical bill pops up, your car needs repairs, or rent goes up again. That’s normal. When it happens, don’t beat yourself up. Adjust the snowball temporarily if you need to, but get back on it as soon as you can.

Track your progress monthly. Write down each debt you knock out. Seeing that list shrink is incredibly powerful. Some people keep a simple notebook or use a free spreadsheet to watch the balances drop.

In 2026, with tools and calculators available online for debt snowball payoff projections, you can even see estimated timelines based on how much extra you can put in each month. It makes the journey feel more tangible.

Building Habits That Last Beyond the Debt

While you’re working the debt snowball, start building small habits that support your new financial life. Track spending for a week to see where money leaks. Cook more meals at home. Find free ways to enjoy time with family instead of spending.

These aren’t about deprivation. They’re about creating space for the life you want after debt. Imagine waking up without that constant worry in the back of your mind. That’s what keeps so many going.

Internal link suggestion: If you’re looking for more ways to boost your income while paying down debt, check out our guide on starting a simple side hustle that fits around your 9 to 5.

Another helpful read might be on creating a realistic budget that actually works for busy lives in 2026.

Also read:- 10 Side Hustles That Are Actually Paying in 2026 and Helping You Finally Break Free From Financial Stress

When to Consider Other Options

The debt snowball isn’t the only path. If your debt feels completely overwhelming, look into consolidation or nonprofit credit counseling. But for most people with manageable but stressful debt, the snowball provides the structure and motivation needed.

Be honest with yourself about what you can sustain. Some months will be stronger than others. That’s okay. Progress over perfection.

Wrapping This Up With Hope

You’ve carried this weight long enough. The debt snowball method offers a practical, human way forward that honors how hard this feels while giving you tools to move through it. Start small. List those debts tonight if you can. Pick one extra action this week, even if it’s just twenty dollars toward that smallest balance.

You are capable of more than you feel right now. I’ve seen it in so many lives, the quiet determination that builds with each small win. Your story can be one of those where 2026 becomes the year things started turning around.

My strong salute to your courage. Keep going, one payment at a time. You’ve got this.

FAQ About the Debt Snowball Method in 2026

1. What exactly is the debt snowball method and how does it differ from other ways to pay debt?

It’s a strategy where you pay off debts from smallest balance to largest, rolling payments forward to create momentum. Unlike methods that focus only on interest rates, it prioritizes quick emotional wins to help you stay consistent.

2. Does the debt snowball method cost more in interest than the debt avalanche method?

Yes, it often does because you might pay high interest debts later. But many people find they actually finish faster overall because the motivation keeps them from quitting. Debt snowball vs avalanche is really about psychology versus pure math.

3. How long does it typically take to pay off debt with the snowball method?

It depends on your total debt, income, and how much extra you can add each month. Some people clear smaller amounts in months, while larger debts take a few years. Using online calculators for 2026 projections can give you a personalized timeline.

4. Can I use the debt snowball if I have student loans mixed with credit cards?

Absolutely. List all debts together by balance size. Make sure to keep minimum payments current on federal student loans to avoid any issues, but apply extra to the smallest balance first.

5. What if I can’t find extra money for the snowball right now?

Start where you are. Even ten or twenty dollars extra helps build the habit. Look for small cuts or one gig shift a week. Momentum grows as you go.

6. Is the debt snowball method still relevant in 2026 with high living costs?

More than ever. With credit card debt totals over a trillion dollars and many facing rent pressure, the psychological boost from small wins helps people stay committed when times are tight.

My warmest salute to you for even reading this far. Taking the first step toward understanding your options shows real strength. Whatever your situation looks like today, know that change is possible, one snowball roll at a time. You’ve got more resilience in you than you realize. Take care of yourself as you move forward.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.

1 thought on “Feeling Stuck With Debt in 2026? Why the Debt Snowball Method Might Be the One Thing That Finally Works for You”