You know that sinking feeling when the email arrives and your monthly student loan payment suddenly looks nothing like what you budgeted for. Your chest tightens, your mind races with questions, and for a moment you freeze. I have seen this look on so many faces over the years. Right now, millions of you are living it as the SAVE student-loan repayment plan comes to its end.

If you are one of the roughly 7 million borrowers who relied on SAVE for those more manageable payments, you are not alone in feeling the panic and confusion. The plan that promised lower monthly amounts and a faster path to forgiveness is being phased out following a court-approved settlement. Borrowers are being asked to switch plans, with servicers set to send notices starting in July 2026 and giving you at least 90 days to choose something new. For many, this shift means higher payments at a time when rent, groceries, and everyday costs already stretch a 9-to-5 paycheck thin.

You might be feeling overwhelmed, wondering how you will keep making progress without getting buried. I understand. I have walked alongside enough people carrying heavy debt loads to know this moment can feel like the ground shifting under your feet. But here is what I want you to hear first: this change, while challenging, does not have to define your future. You still hold the power to take clear, steady steps forward. In the pages ahead, we will walk through what is happening, what your real options look like, and most importantly, how you can protect your peace of mind and build real momentum again.

The Human Side of the End of SAVE Repayment Plan 2026

Let me speak to your heart for a moment. You went to school because you wanted a better life for yourself and your family. You signed those loan papers with hope, not with any intention of dodging responsibility. Now the rules are changing mid-stream, and suddenly the numbers do not add up the way they once did. One borrower I read about recently described staring at her new projected payment and feeling her body go cold. She has a good state job in environmental work, yet that jump in monthly obligation made her wonder if Public Service Loan Forgiveness would stay within reach.

You might be in a similar spot. Maybe you are a project manager who counted on those lower SAVE payments to cover rent in a high-cost city. Or perhaps you are a parent watching every extra dollar disappear before it can go toward retirement or your kids’ needs. These feelings of panic are real and valid. I have seen how debt stress can quietly steal your sleep and dim your sense of possibility.

Yet I have also seen something else. I have seen ordinary people, just like you, face similar shocks and still find a way to breathe, adjust, and keep moving. The key is refusing to let fear freeze you in place. You deserve a plan that respects both the reality of your loans and the dreams that got you here in the first place.

What the End of the SAVE Student-Loan Repayment Plan Really Means for Your Wallet

The SAVE plan offered some of the lowest monthly payments among income-driven options and faster forgiveness timelines for many. With its elimination, payments for some borrowers could rise significantly, sometimes doubling or more depending on income and loan balance. For a person earning around $77,000 with substantial loans, that difference can feel like needing a second job just to stay afloat.

Interest will start accruing again for many who were in forbearance, and the previous protection against negative amortization is no longer the same. The Department of Education is encouraging early switches to give you time to adjust your budget. That is practical advice, but I know it is easier said than done when life already feels full.

Here is what matters most right now: you do not have to figure everything out in one panicked evening. Take one breath, then one small action. Log into your account on StudentAid.gov and review your current balance and servicer details. Knowledge is the first light in the darkness.

Student Loan Repayment Changes July 2026: What Is Coming and When

July 2026 marks a turning point. Starting then, loan servicers will begin contacting SAVE borrowers with specific 90-day windows to select a new plan. If you do not choose, you may be moved automatically to the Standard plan or the new Tiered Standard Plan.

At the same time, the Repayment Assistance Plan (RAP) launches on July 1. This new income-driven option will eventually become the primary one for many borrowers, especially those taking out fresh loans after that date. Existing borrowers have a bit more flexibility until 2028, but acting sooner can prevent surprises.

These changes stem from the One Big Beautiful Bill Act and the settlement ending SAVE earlier than the original 2028 timeline. The goal from the administration’s perspective is simpler, more sustainable repayment that honors the original loan obligation. For you, it means preparing your budget for potentially higher payments while exploring what still fits your life.

You might ask yourself right now: “Am I ready for this shift, or do I need more time to understand my choices?” That honest question is a good starting point. Many of you balancing a 9-to-5 with gig work like DoorDash or Uber already know how to stretch a dollar. Those same skills will serve you here.

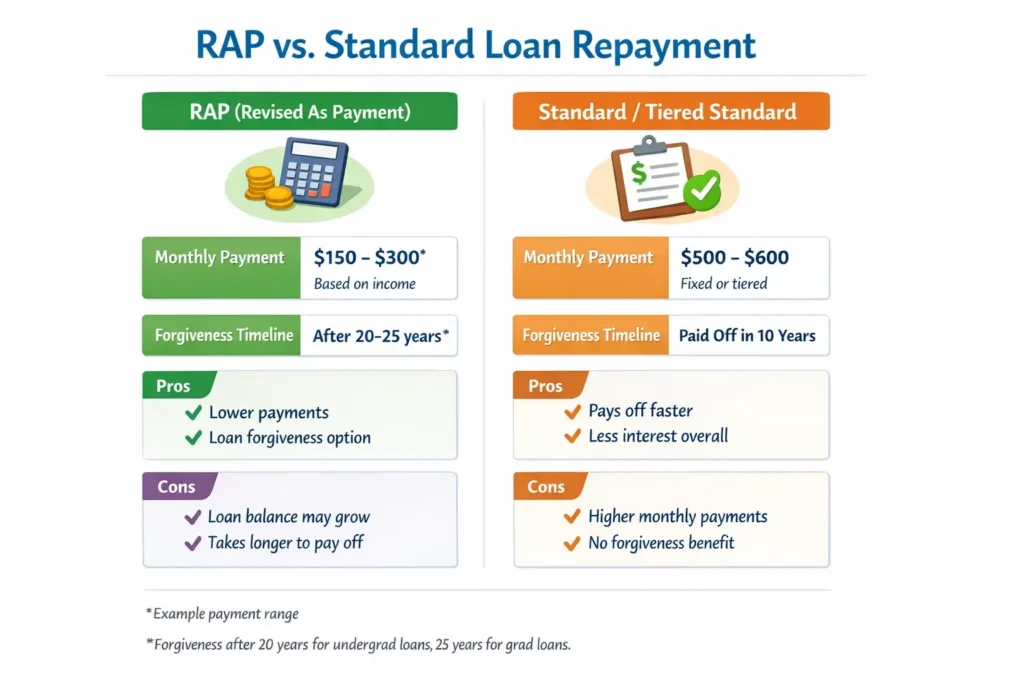

New Repayment Assistance Plan (RAP) vs Standard Plan: A Clear Comparison

Let’s break this down simply and honestly so your mind can settle on the facts.

The Standard Plan (or new Tiered Standard) is fixed-payment. Payments stay the same each month, and the term is usually 10 to 25 years depending on your total debt. It is straightforward but can feel heavy if your income is modest or variable.

The Repayment Assistance Plan (RAP), launching July 1, 2026, is income-driven. Payments are generally calculated as a percentage of your adjusted gross income, starting as low as $10 for very low earners and scaling up to 10 percent for higher incomes. It includes a $50 monthly reduction per dependent child and aims to prevent your balance from growing unchecked due to unpaid interest.

Key differences you will want to weigh:

- RAP tends to offer lower monthly payments for lower- and middle-income borrowers compared to a fixed Standard plan, but the forgiveness timeline stretches to 30 years for many (versus shorter periods under older IDR plans).

- Standard plans may pay off the debt faster if you can afford the fixed amount, but they do not automatically adjust if your income drops.

- For those pursuing Public Service Loan Forgiveness, staying on a qualifying income-driven plan like RAP remains important.

Many borrowers tell me the choice comes down to cash flow today versus total cost and timeline tomorrow. Run the numbers on the official Loan Simulator tool at StudentAid.gov. It is free and can show you personalized estimates.

Here is one real-life example that might sound familiar. Sarah, a teacher in the Midwest earning about $55,000, saw her SAVE payment jump from under $200 to over $600 under a standard plan. She switched to an available income-driven option early and started driving for Uber on weekends. That extra $400–600 a month helped bridge the gap while she kept qualifying payments ticking for PSLF. She felt scared at first, but the small wins built her confidence.

Another borrower, Marcus, a freelance graphic designer in a big city, used the transition as a reason to finally organize all his finances. He added freelancing clients through Upwork and cut a few subscription services. His new RAP payment, while higher than SAVE, still left room for progress on credit card debt he had been carrying.

Your story may look different, but the pattern is the same: small, consistent actions create breathing room.

How to Switch Student Loan Plans Before the July Deadline

You do not have to wait for the email. If you are on SAVE now, you can contact your servicer today or apply online through StudentAid.gov to move to another qualifying plan. The process usually involves submitting an income-driven repayment application and providing consent for the Department to pull your tax data directly from the IRS for faster processing.

Steps that help most people:

- Log into StudentAid.gov and review your loans and current plan.

- Use the Loan Simulator to compare options.

- Submit the IDR application if an income-driven plan fits best.

- Keep records of every submission and confirmation.

- Set calendar reminders for recertification dates once approved.

If you are pursuing PSLF, make sure the new plan still qualifies. Acting before the busy July period can give you more time to adjust your budget and avoid any administrative delays.

You might be wondering, “What if I make the wrong choice?” That is a fair and human question. Start with what protects your monthly cash flow without sacrificing long-term progress. You can always adjust later in most cases.

Internal Link Suggestion: If you are looking for more on managing multiple debts, check out our guide on balancing student loans with credit card payoff strategies.

Side Hustles and Smart Moves to Ease the Pressure

When payments rise, many of you turn to the gig economy for extra income, and that instinct is wise. Driving for Uber or DoorDash a few evenings a week, delivering through apps, or offering freelance services online can create a buffer. One borrower I know added $800 monthly by tutoring students online in the evenings after her 9-to-5.

Beyond hustles, look at your full budget with fresh eyes. Track where every dollar goes for two weeks. Small cuts, like brewing coffee at home instead of buying daily, or negotiating a lower rent when your lease renews, add up. Consider consolidating high-interest credit cards if rates allow, freeing up money for your student loans.

The goal is not perfection. It is creating enough margin so the loan payment does not bury you emotionally or financially.

Is Student Loan Forgiveness Taxable in 2026?

This is an important shift to understand. The temporary provision that made most federal student loan forgiveness tax-free expired at the end of 2025. Forgiveness received in 2026 or later under many income-driven repayment plans may now be treated as taxable income by the IRS. You could receive a Form 1099-C and need to report it on your tax return.

Important exceptions exist. Forgiveness under Public Service Loan Forgiveness generally remains non-taxable. Certain other discharges like Total and Permanent Disability also have protections. Always check with a tax professional for your specific situation, as state rules may differ.

Factor this into your planning. If you are close to forgiveness, speak with a qualified advisor about setting aside funds for potential taxes. Knowledge here prevents nasty surprises next filing season.

Also read:- Don’t Wait for July 2026! 7 Critical Student Loan Steps You Must Take Before the SAVE Plan Ends

Turning Uncertainty Into Lasting Financial Strength

You have already shown strength by getting this far. The end of the SAVE student-loan repayment plan does not erase your efforts or your worth. It simply asks you to adapt, and adaptation is something human beings do remarkably well when we support one another and take things one step at a time.

Ask yourself these gentle questions: What is one small action I can take this week to understand my options better? How can I bring in even $100 extra this month to build a cushion? Who in my life can I talk to for encouragement?

You are capable of more than you feel in this anxious moment. Many people have walked through debt transitions and emerged with clearer finances, stronger habits, and renewed hope. You can too.

If this article resonates, take that first step today. Log into your account, run the simulator, or reach out to your servicer. Momentum begins with movement, however small.

My warmest salute to every borrower reading this who refuses to let today’s confusion steal tomorrow’s possibilities. You are showing up, you are learning, and that matters deeply. Keep going, friend. Better days are built one honest choice at a time.

FAQs

What exactly is happening with the SAVE student-loan repayment plan in 2026?

The SAVE plan is ending following a court-approved settlement. Borrowers are being transitioned to other legal repayment plans, with notices and 90-day choice periods beginning in July 2026.

When do the main student loan repayment changes July 2026 take effect?

The Repayment Assistance Plan (RAP) and other new options become available July 1, 2026. Servicers will contact SAVE enrollees around that time with instructions to switch within 90 days.

How does the New Repayment Assistance Plan (RAP) compare to the Standard Plan?

RAP bases payments on income with a minimum of $10 and adjustments for dependents, while the Standard Plan uses fixed payments over a set term. RAP often helps with affordability but may extend the overall repayment timeline.

How can I switch student loan plans before the July deadline?

You can apply now through StudentAid.gov or your servicer. Use the IDR application and consider consenting to IRS data retrieval for faster processing.

Is student loan forgiveness taxable in 2026?

For many income-driven forgiveness amounts received in 2026 or later, yes, it may be treated as taxable income. PSLF forgiveness generally remains non-taxable. Consult a tax advisor.

What should I do if my payments are about to skyrocket?

Review your budget, explore available repayment plans via the Loan Simulator, consider qualifying side income, and act early to switch plans if needed. Small daily choices compound.

Will I still qualify for Public Service Loan Forgiveness after switching?

As long as you move to a qualifying plan like RAP (for eligible borrowers), your previous qualifying payments should continue to count toward PSLF. Verify with your servicer.

Disclaimer: This article is for educational and informational purposes only. It is not financial, investment, or legal advice. Always consult a qualified financial advisor before making any financial decisions.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.