That moment when you wake up and realize the debt is still there? Yeah, I know that feeling. Your chest gets tight. You haven’t even had coffee yet, and you’re already carrying the weight of credit card statements, student loans, overdue medical bills. It’s exhausting in a way that’s hard to explain to people who don’t live it.

About one in four Americans decided 2026 is the year they’re finally going to break free from this. That’s a lot of people lying awake at night just like you are.

Debt creeps up on you in the most ordinary ways. You had an unexpected hospital bill. Your car needed work. Maybe you lost a job for a few months and had to lean on credit cards to stay afloat. Nobody wakes up thinking “I’m going to be in debt forever.” It just happens. And then one day you add it all up, and the number is so big it doesn’t even feel real anymore.

The good news? You can genuinely get out of this. Not through some miracle or a lottery ticket, but through actual strategy and showing up consistently, even when it’s boring or hard. And honestly, the goal isn’t just about eliminating the numbers. It’s about getting your life back from the stress of carrying this around every single day.

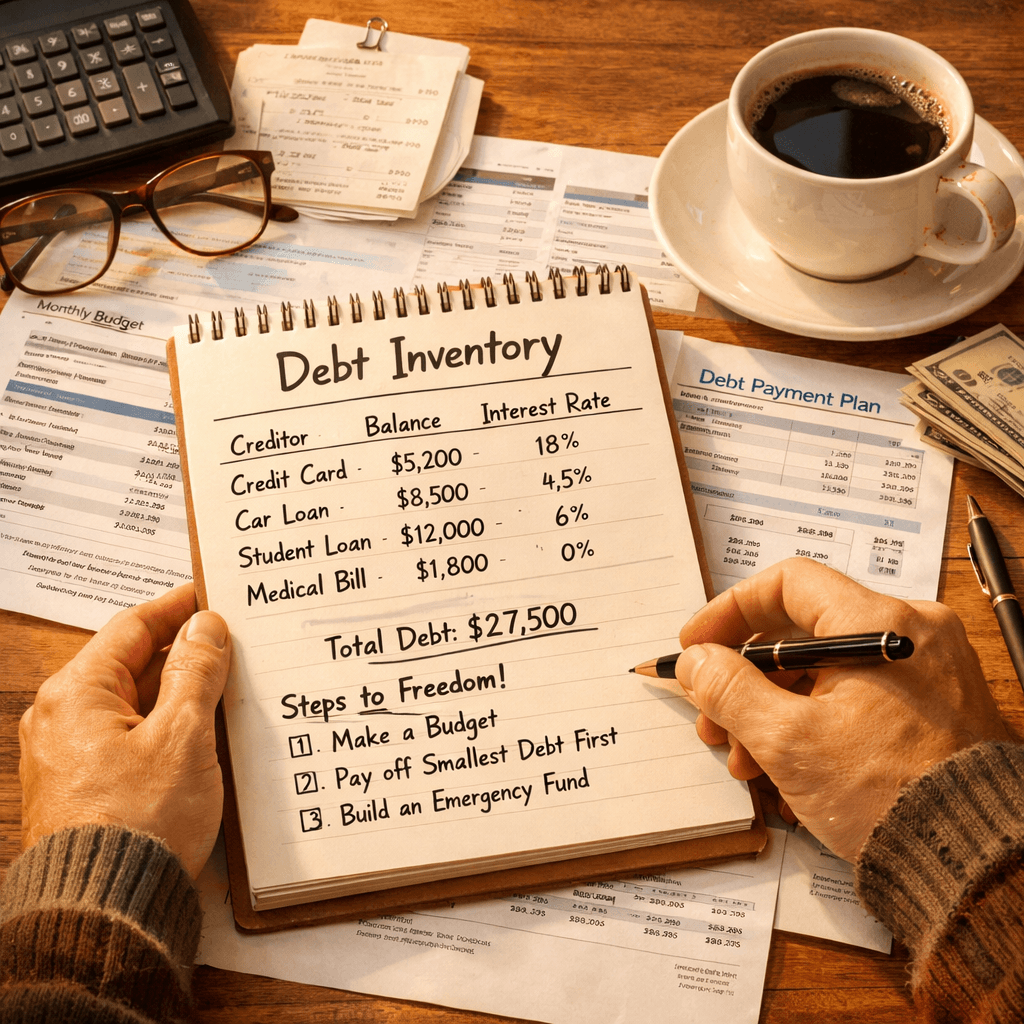

1. Know Exactly What You Owe (Because You Can’t Fight What You Don’t See)

Most people avoid this step. I get it. There’s something almost easier about not knowing the exact number. You can almost pretend it’s not as bad as you fear. That works until it doesn’t.

The debt doesn’t disappear when you’re not looking at it. It just sits there, gathering interest like frost accumulating on a cold morning.

So. You’re going to sit down with coffee or tea or whatever gets you through hard moments. Find somewhere quiet where nobody’s going to interrupt you. And you’re going to write down every single debt you have. This sounds simple, but most people have never actually done it.

Here’s what you’re tracking:

Each credit card balance and what you’re being charged in interest Student loans (federal and private) Auto loans, personal loans, anything else you owe Medical debt yeah, that stuff counts Those buy now, pay later things that seemed harmless at the time

For each one, write down:

The actual balance right now The interest rate (the APR) Your minimum monthly payment When it’s due

This inventory isn’t to make you feel worse. Trust me, I’ve watched people do this a thousand times. What actually happens is the opposite. You get clarity. Suddenly the fog lifts. The problem becomes solvable instead of just this vague scary thing hanging over you.

Sarah, who works as an accountant in Michigan, was carrying debt across 11 different credit cards. Eleven. She kept trying to tackle it without writing anything down, and it wasn’t working. When she finally sat down and made that list, the number was $28,500. But here’s what really woke her up: she was paying $890 just in interest every single month. Not toward the actual debt. Just interest. That’s when it clicked. That number made it real. That number made her ready to actually fight back.

Marcus, a delivery driver in Texas, discovered something similar when he listed everything. Three store credit cards, all charging him 24% APR. He had no idea they were that expensive. Seeing them listed out side by side? That changed everything about his approach.

2. Choose Your Battle Strategy: Snowball vs. Avalanche

Okay, so you know what you owe. Now comes the decision about how you’re going to attack it. There are two main approaches, and they’re different enough that the choice actually matters based on how your brain works and what keeps you motivated.

The Debt Snowball Method: Building Momentum

This one’s all about psychology. You list your debts from smallest balance to largest, and you don’t care about interest rates. Zero consideration. You make minimum payments on everything except the smallest balance. That smallest one? Everything extra goes there.

When you finally kill that first debt, you take the payment you were throwing at it and add it to the next smallest debt. It’s like rolling a snowball down a hill it gets bigger and bigger as it goes.

Why does this work for so many people? Because small wins matter. A lot. Pay off that first card in two or three months, and something shifts inside you. You feel it. You actually did something. And that feeling carries you through the longer, harder battles coming down the road.

The Debt Avalanche Method: The Math-First Approach

This method is about playing the long game with numbers. You find the debt with the highest interest rate and attack that first. Minimum payments on everything else, but extra money goes to the beast with the biggest teeth.

Once that’s gone, you move to the next highest rate. Mathematically, you’ll spend less total money and get free faster. If you’re the type of person who loves seeing the efficiency, this is your strategy. The numbers don’t lie.

Here’s my honest take: the best method is the one you’ll actually stick with. Not the one that sounds good in theory. Not the one a financial expert told you about. The one you’ll keep doing in March when progress feels glacial. The one you won’t abandon in July because you’re tired. The one that keeps you going.

For most people just starting out, I’d lean toward the snowball. Get that first win quick. Feel it. Then build from there. You can always shift strategies later once you know you’ve got this.

3. The Debt Consolidation Option: When Combining Makes Sense

Sometimes, the smartest move isn’t paying off your debt as it exists. Sometimes it’s restructuring it entirely through consolidation. This is especially true if you’re juggling multiple high-interest debts, particularly credit cards.

Think of consolidation like this: instead of making eight different payments to eight different creditors, you make one payment to one creditor. Instead of paying an average of 21% interest on credit cards, you might pay 12% on a consolidation loan. That’s real money saved every month.

Balance Transfer Credit Cards

A balance transfer card offers a 0% APR for a limited time, usually 12 to 21 months. During that period, every dollar you pay goes directly to principal instead of interest.

Let’s look at real numbers. If you have $8,000 in credit card debt at 21% APR, and you pay $300 monthly, you’ll pay about $2,500 in interest before the debt is gone. With a balance transfer card at 0% APR for 21 months, paying the same $300 monthly, you’d be completely debt-free in 27 months and pay zero dollars in interest.

The catch? There’s usually a balance transfer fee of 3% to 5%, and you have to actually pay off the balance before that 0% period ends, or you’re right back to high interest rates. You also need decent credit to qualify.

Debt Consolidation Loans

With a consolidation loan, you borrow enough to pay off multiple debts at once, then you pay off that single loan. Pretty straightforward. The benefits:

One interest rate that stays the same One payment instead of juggling multiple Usually better APRs than credit cards A repayment schedule you can actually plan around

You won’t get 0% like a balance transfer card offers, but 6% to 14% beats the hell out of 21%. And honestly? The psychological win of one payment instead of five is huge. It’s so much easier to stay consistent when you’re not managing multiple due dates and companies.

Marcus had those three store cards and a regular credit card that were killing him. He rolled them all into a single consolidation loan at 9.5% APR. His new payment was $420, which was actually lower than what he’d been paying across all the accounts because the rate was better and he had a longer timeline. That extra breathing room in his monthly budget made all the difference. It wasn’t magic. It was just simpler.

When This Makes Sense (and When It Doesn’t)

Consolidation works when:

You’ve got multiple high-interest debts dragging you down Your credit score is decent enough (650 or higher usually) You’re actually going to stop running up new debt while you pay this off The numbers work out the lower interest rate saves you money even with any fees involved

It probably won’t help if:

Your credit is really damaged You know yourself well enough to know you’ll just max out those cards again You’re hoping for a quick fix instead of actually changing your habits

4. The Side Hustle Reality: Making Extra Income Work for You

Budgeting alone? That takes forever. You need a budget, sure. But what you really need is more money. Specifically, you need to be willing to dedicate some of your free time to actually accelerating this debt payoff instead of just doing the minimum.

That’s where side hustles come in.

Most people with a side gig make somewhere between $300 and $1,000 monthly in extra money. That’s almost $4,000 to $12,000 in a year that didn’t exist before. If you throw that at debt instead of lifestyle inflation, you’re not just making progress. You’re actually changing when you’ll be free.

Also read:- 10 Side Hustle Ideas for Building Emergency Funds That Actually Work in 2026

What Actually Works

The trick to picking a side hustle is matching it to your actual life, not some fantasy version of yourself. You need something that:

Fits around your day job without destroying you Doesn’t require a bunch of startup money Uses skills you already have (or can quickly develop) Actually starts putting money in your pocket relatively soon

Delivery Driving (Uber, DoorDash, Instacart, Amazon Flex)

This is the fastest way to start making money basically today. You need a reliable car and a valid driver’s license. That’s it. Your hourly varies by location and what time you’re working, but lunch and dinner hours consistently pay better. Most drivers are looking at $15 to $25 per hour after expenses. Even if you just work 10 hours a week, that’s $600 to $1,000 monthly that can go straight to debt.

Freelance Writing, Design, Web Work

Companies need writers, designers, and people who know their way around web stuff. Platforms like Upwork, Fiverr, and various specialty job boards connect you with people who need this work. A freelance writer might make $50 to $300 per article. A graphic designer could charge $200 to $1,000 for a project. The income potential is genuinely unlimited if you build a decent client base.

The downside is it takes a little time to ramp up. Your first month might be slow. But once you’ve got a couple of reliable clients, maybe even one paying you $400 to $800 monthly for ongoing work? That changes everything.

Online Tutoring

If you’re good at any subject, there are students who need you. Math, English, science, test prep, teaching English to international students. Tutoring pays around $20 to $50 per hour. Five to 10 hours a week gets you $400 to $2,000 monthly.

Selling Stuff You Don’t Need

Not a long-term solution, but it’s real money. Go through your house. Honestly. You probably have $500 to $2,000 in stuff you’ve forgotten about. List it on Facebook Marketplace, eBay, Poshmark. That’s one debt payment right there. Maybe two.

Renting Out Space or Extra Assets

If you’ve got an extra parking space, a storage corner, or an unused room, you can rent it. Short-term rentals on Airbnb bring in $500 to $2,000 monthly depending on where you live. A parking spot might be $50 to $200. It’s passive income that doesn’t require much from you.

The Critical Rule Nobody Follows

Here’s where most people sabotage themselves: they earn extra money and then it just… vanishes. They buy something they don’t need. They go out more. The extra income disappears into thin air.

Don’t let that happen.

Open a separate bank account just for side hustle money. The moment that money hits your checking account, transfer it over. Make it a rule: side hustle income has one job and one job only. Debt payoff. No exceptions. No “I’ll just spend a little on myself.” No small purchases. It all goes to debt.

Jennifer is a good example of this. She started doing freelance writing in her spare time while her kids were at school. First month? $280. Second month, $450. By month six, she had steady clients and was making $1,200 monthly. Every single dollar went to her credit cards. She paid off $7,200 in the first year without any major lifestyle changes. Still got her coffee. Still spent time with her kids. But she was making real progress.

5. Budget Cuts That Don’t Feel Like Punishment

Here’s the thing about budgeting: most people hate it because most budgets feel like you’re punishing yourself. You’re told to give up coffee, never eat out, have zero fun. It feels like deprivation, so you quit after a month.

Let’s try a different approach. Instead of thinking about it as budgeting, think about it as being intentional with your money. You’re not depriving yourself. You’re making conscious choices about where your limited dollars actually matter to you.

Find the Easy Wins First

Before you cut anything big, look for the low-hanging fruit:

Subscriptions you’ve forgotten about. Most people have at least three to six subscriptions they’re not actually using. That’s easily $30 to $100 monthly you’re just throwing away. Cancel the streaming services you’re not watching. Drop that gym membership you haven’t used since January.

Call your utility and insurance companies. Seriously. Tell them you’re shopping around for better rates. A lot of the time, they’ll match or beat competitor pricing just to keep you. These conversations typically save $20 to $50 monthly.

Cook more, eat out less. This is where most people find the biggest wins. If your family spends $200 monthly on takeout and restaurants, cutting that to $50 through meal planning? That’s $150 monthly, or $1,800 per year, going straight to debt. You’re not eating sad salads. You’re just being intentional about when and where you spend on food.

The 50/30/20 Framework Actually Works

One budget system that doesn’t feel awful: 50% of your after-tax income on needs. 30% on wants. 20% on debt and savings. When you’re in debt-crushing mode, flip it to 50/20/30. You’re still living your life. You’re just putting more toward your future.

The beauty of this approach is it doesn’t eliminate everything you enjoy. It just makes sure enjoyment doesn’t consume your entire financial picture.

What Actually Sticks

The spending cuts that work long-term are the ones you can actually live with. If coffee is your daily anchor, buy your coffee. If spending time with friends matters to you, keep that. Don’t cut what you love. Instead, cut what you don’t actually care about.

For some people, that’s eating out. For others, it’s expensive hobbies. For someone else, it’s premium cable. Figure out what you genuinely don’t value that much, and that’s where you cut.

6. Automate Your Way to Consistency

Here’s a truth that matters: willpower is not reliable. Some days you wake up and you’ve got tons of it. Other days? It’s just gone. You can’t build a debt payoff plan on willpower alone. You need systems that work even when you’re tired or discouraged.

The easiest system is automation.

Set up automatic payments for more than the minimum on your target debt. If you’re using the snowball method and attacking your smallest debt first, make sure $500, $750, whatever you can actually manage, goes out automatically on the tenth or the 25th of each month. You can’t talk yourself out of it. You can’t decide to spend it on something else. The money just goes.

Why does this work? Because you forget. Because willpower is fragile. Because on the day it’s due, you’re tired and hungry and you’d rather not think about it.

The same goes for side hustle income. Set it up so that money goes directly to your debt account the moment it clears. No waiting for you to decide what to do with it. It moves automatically.

Some people have good luck with apps that round up their purchases and send the difference to debt. You spend $4.50 on coffee, and an extra fifty cents goes toward your debt. It seems tiny, but $10 to $20 monthly from rounding adds up to $120 to $240 annually. That’s real.

7. Handle the Emotional Side of Debt Payoff

Nobody really talks about this, but here’s the reality: the emotional journey of paying off debt is just as important as the financial strategy. Maybe more.

In the beginning, there’s relief. You’ve got a plan. You know what to do. You feel like you can finally breathe.

But then you hit the middle section, and that’s where it gets hard. You’ve paid off maybe $5,000 of $30,000. It’s real progress, but it still feels like you’re moving a mountain with a teaspoon. This is where people quit. Not because the strategy doesn’t work, but because the motivation dries up.

Then there’s the shame that a lot of people carry about being in debt in the first place. And I want you to hear this: it’s not your fault. This is how the system works. This is normal life. Most Americans carry debt. That doesn’t make you weak or stupid. It makes you human.

Reframe How You Talk to Yourself

Instead of “I have this horrible debt problem,” try “I’m solving something that took years to create, and I’m doing it methodically and intelligently.”

Instead of “I’m so dumb for getting into this,” try “I made decisions based on what I had at the time, and now I’m making better decisions.”

The words you use when talking to yourself matter. You’re not a failure. You’re not irresponsible. You’re someone in the middle of a correction, and corrections take time.

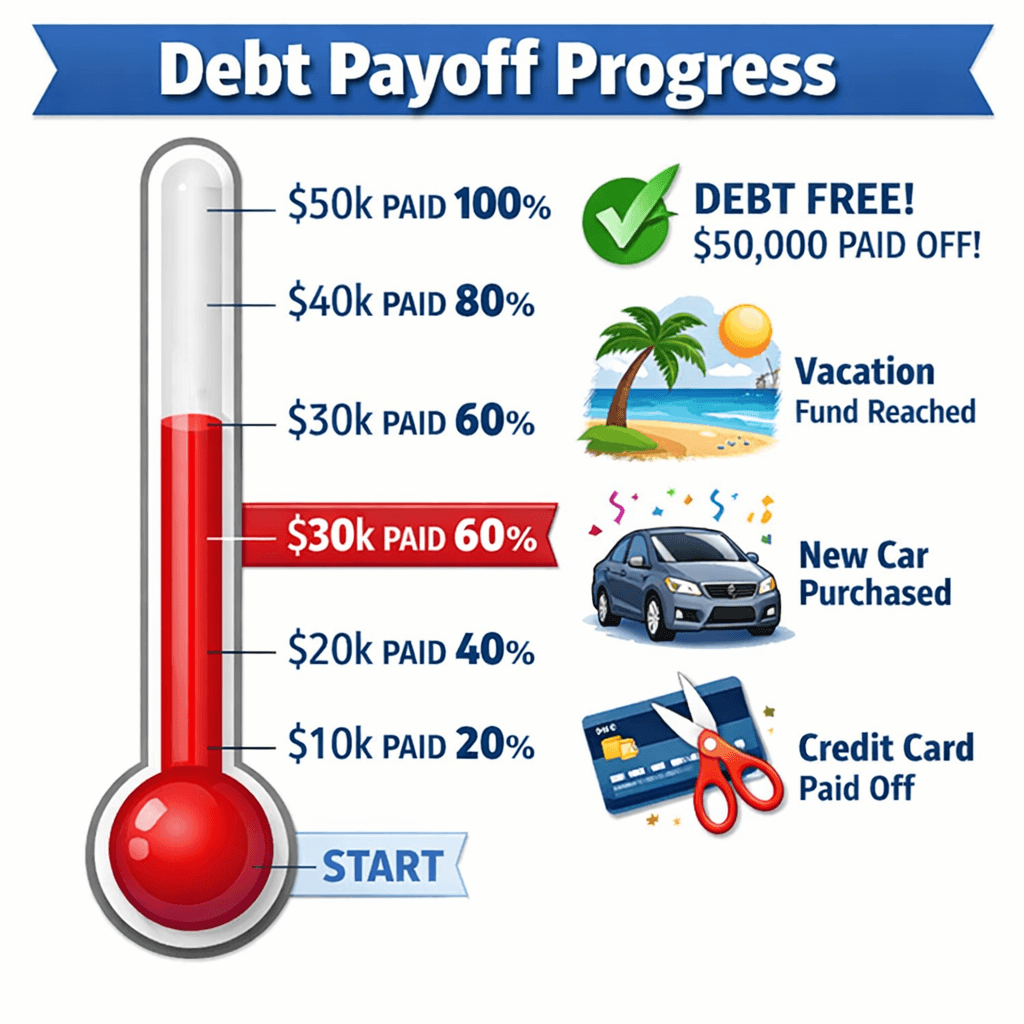

Make Your Progress Visible

Keep track of what you’re doing. Use a visual tracker. Cross off amounts. Update your spreadsheet. Some people print out a thermometer graphic and fill it in as they reach milestones. Seeing that visible progress keeps motivation alive during the hard middle.

Celebrate the wins. When you pay off that first card or hit $5,000 paid off, take a moment and actually feel it. You did that. You made that happen. That’s not small.

Professional Help Is Okay

If the debt feels genuinely overwhelming, or if you’re struggling with the psychological weight of it, there’s no shame in getting professional support. Non-profit credit counseling agencies (affiliated with the National Foundation for Credit Counseling) offer free or low-cost guidance. They can help negotiate with creditors and sometimes set up debt management plans that reduce your interest rates.

Companies like Freedom Debt Relief work with people who have significant debt loads. These aren’t quick fixes, but they’re real options when you need real help.

Just be careful: work with accredited, non-profit organizations. Avoid anything that promises instant debt erasure or charges huge upfront fees.

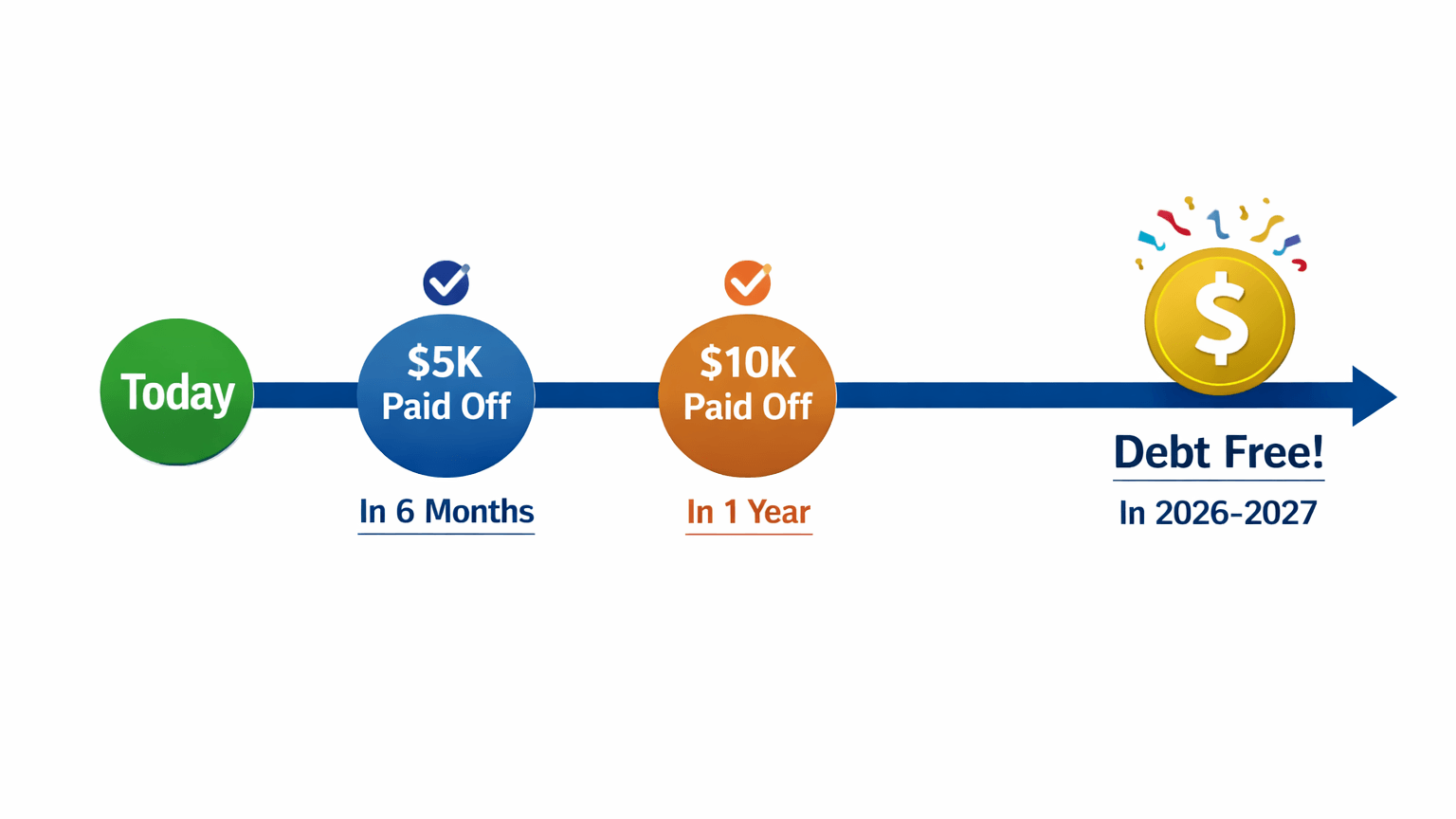

Your 2026 Debt Freedom Timeline

Having a realistic timeline matters. It makes this abstract goal actually concrete.

Let’s say you’ve got $20,000 in debt. What would it actually take to get free?

Using the snowball method with an extra $500 monthly beyond minimum payments? You’re looking at roughly 2 to 2.5 years. So December 2027 or early 2028.

But if you find a side gig that brings in $500 monthly and you direct all of it to debt? Your timeline cuts in half. You could be debt-free by end of 2026 or early 2027.

Consolidate that high-interest debt from 21% down to 9%? Your interest payments drop like a rock, and more of each dollar actually goes toward the principal instead of enriching the credit card company.

That’s how you actually change the timeline. Not through some magical motivation. Through strategy.

Real-Life Examples That Matter

Let me share three real stories. The names have changed, but everything else is exactly how it happened.

Sarah’s Snowball Success

Sarah is 34 and works as an accountant in Michigan. She had 11 credit cards. Eleven. And $28,500 spread across them. She was paying $890 monthly just in interest. Just in interest. Not toward the actual debt.

When she finally listed everything out (smallest balance to largest), her smallest card had $1,200 on it. She decided to attack that one aggressively while keeping minimum payments on everything else. She also made a bunch of phone calls to negotiate her interest rates. She got lucky on three cards they dropped rates by 2% to 4% just for asking.

Six months later, that first card was paid off completely. That momentum hit her hard. She added that payment to the next smallest card and kept going. Within three years, through consistent effort and refusing to add new debt, she was completely credit card free. That $890 monthly interest payment became zero. Now she’s finally building an emergency fund.

Marcus’s Delivery Solution

Marcus is 29 and drives for his main job, making about $38,000 a year. Stable, but not generous. He had $12,000 in personal loans and credit cards spread across four accounts.

Instead of cutting his already-lean budget, he picked up delivery work at night and on weekends. DoorDash, mostly. His car was paid off, so his only extra expense was gas. He averaged about $18 per hour after expenses.

He committed to 15 hours per week. That’s $270 weekly, around $1,080 monthly. Every dollar went to debt. Within 12 months, he’d paid down nearly $13,000. Combined with his regular minimum payments, he was completely debt-free. Now that $1,080 monthly is going into savings and investments.

Jennifer’s Freelance Leap

Jennifer is 31, a stay-at-home mom with two kids. She had $16,000 in student loans and credit card debt. Zero extra money in the budget. She couldn’t take a traditional job because childcare costs would have eaten her entire salary.

She started freelance writing on Upwork and Contently during naptime and after the kids went to bed. First month was $280. Month three was $800. By month six, she had steady clients and was making $1,200 monthly in side income.

She kept her budget tight and directed every freelance dollar to debt. Two years later, she was completely debt-free. Now she works freelance part-time and is actually ahead financially. Her kids get her and she get to work from home. That’s not a bad outcome.

These three people didn’t have anything special going for them. No inheritance. No huge salary increase. No luck. They just had a plan and stuck with it.

Frequently Asked Questions About Paying Off Debt in 2026

Q: I have almost no money left after bills each month. How can I possibly pay off debt faster?

A: This is when side hustles become critical. Even just 5 to 10 hours per week of extra work can generate $200 to $400 monthly that goes straight to debt. Start with whatever has the lowest barrier to entry: selling stuff you don’t need, pet sitting, delivery work. These start generating income immediately. As you build skills, you can move into higher-paying work like freelancing.

Q: Should I pay off debt or build an emergency fund first?

A: Both, actually. Save enough to cover a small emergency ($1,000 to $2,000) first so an unexpected expense doesn’t send you back into debt. Once you’ve got that cushion, go after the debt aggressively. After that’s mostly gone, then build your emergency fund to three to six months of expenses.

Q: What’s the difference between debt consolidation and debt relief?

A: Consolidation combines multiple debts into one, usually with a better interest rate. You’re still paying the full amount owed, just through a different structure. Debt relief involves negotiating with creditors to pay less than you actually owe. Relief does more damage to your credit but can be necessary when you genuinely can’t pay the full amount.

Q: Is it better to use a balance transfer card or a consolidation loan?

A: Balance transfer cards work better if your debt is under $8,000 to $10,000 and you’re confident you can pay it off during the 0% period. Consolidation loans make more sense for larger debts where a longer timeline makes sense, even with some interest.

Q: Can I really become debt-free in 2026?

A: Depends on your situation. If you have under $5,000 in debt and you’re aggressive about it, probably yes. If you have $50,000 in debt on a $40,000 salary, realistic timeline is 2 to 3 years. But you can make massive progress in 2026 regardless of your situation.

Q: How do I stop myself from running up new debt while paying off old debt?

A: This is critical. Delete your credit card apps from your phone. Use cash or debit cards for spending. Set alerts on your accounts. Most importantly, figure out why you accumulated debt in the first place. Was it emergency spending? Lifestyle inflation? Understanding the root helps prevent it from happening again.

Q: What if I have debt in collections or past due?

A: Stop the bleeding first. Contact the creditor or collection agency and arrange a payment plan. Get something in writing. Then aggressively pay down this high-priority debt because it’s damaging your credit most. Collections debt should be your highest priority after your current minimum payments.

Q: Should I close credit cards once I pay them off?

A: Not right away. Closing cards can hurt your credit score by reducing your available credit. Once the debt’s gone, keep cards open but paid off. Just don’t use them for new purchases.

Your Personal Commitment

I want to come back to something important. You’re not broken because you have debt. You’re not behind because you’re starting this journey now. You’re definitely not alone. One quarter of Americans made this same commitment you’re making right now.

The real question is whether you’ll stick with it.

Paying off debt in 2026 isn’t about motivation during the exciting moments. It’s about showing up in March when progress feels slow. It’s about staying committed in July when you’re tired and nothing feels like it’s working. It’s about not giving up in September because one month felt too tight.

It’s about recognizing that this is a long game, not a sprint. And long games are won by people who just keep moving forward, one day at a time.

You’ve got the strategies now. You know snowball and avalanche methods. You understand consolidation. You have three real examples of people who actually did this. You know where to find side hustle income. You know that budgeting doesn’t mean suffering.

What happens next is completely up to you.

I’d encourage you to take one action this week. Just one. Pick your debt payoff method and write down which debts you’re tackling. Or open a separate account for side hustle money if you’re going to pursue extra income. Or make one phone call to negotiate a better interest rate.

One action. That’s how you start.

Because this time next year, you could be telling someone you love that you paid off your first $5,000. Or $10,000. Or maybe way more. You could be describing what it felt like to finally see real progress against something that felt impossible when you started.

That story starts today. It starts with you deciding this matters and taking one small step forward.

I genuinely believe this is possible for you. I’ve watched people do it, and I see no reason it can’t be you next.

Disclaimer: This article is for educational and informational purposes only. It is not financial, investment, or legal advice. Always consult a qualified financial advisor before making any financial decisions.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.

1 thought on “7 Real Ways to Pay Off Debt in 2026: Your Complete Roadmap Out of Financial Stress”