I understand where you are right now. You’ve been managing your student loans as best you can, maybe you’ve heard about the SAVE plan ending, and honestly, the uncertainty feels overwhelming. The news keeps changing, the timelines keep shifting, and you’re wondering what it all means for your monthly budget and your long-term financial plan.

That feeling is real, and it’s exactly why we need to talk about how to prepare for July 2026 student loan changes. These changes are coming whether we’re ready or not, and the truth is that getting informed today could save you hundreds or even thousands of dollars in the months and years ahead.

The landscape of federal student loans is shifting dramatically as we move through 2026. What once seemed like a straightforward path to repayment is now branching into new directions, and you need to understand where those paths lead. Let me walk you through this together so you can make decisions with clarity instead of confusion.

Understanding the SAVE Plan End of July 2026

Let me be clear about what’s happening. The Saving on a Valuable Education (SAVE) plan, which offered some of the lowest monthly payments available to federal student loan borrowers, is coming to an end. More than 7 million people enrolled in SAVE have already been in forbearance for over a year while the legal battle continued, and these borrowers will soon need to transition to other repayment options.

This wasn’t supposed to happen this fast. If you’ve been following the news, you know that the SAVE plan faced legal challenges almost immediately after its launch during the Biden administration. Beginning on July 1, federal loan servicers will notify borrowers that they have 90 days to switch to a new repayment plan. That’s right. If you’re one of those 7.5 million borrowers currently on SAVE, this affects you directly.

Here’s what makes this particularly challenging for many of you. The SAVE plan was designed with a specific promise: reduced monthly payments based on your actual income. Some borrowers with lower incomes were paying zero dollars per month while their loans sat in forbearance. Now that safety net is being pulled away, and the replacement options aren’t quite as generous.

The end of SAVE repayment plan 2026 represents something deeper than just a policy change. It represents a fundamental shift in how the government views student loan relief. Understanding this shift helps you prepare mentally and financially for what comes next.

The 90-Day Deadline: Why You Cannot Ignore This

Let me tell you why I’m emphasizing this deadline so heavily. Borrowers will have 90 days starting on July 1, 2026, to select another repayment plan, the U.S. Department of Education said in its statement. Loan servicers will communicate specific deadlines to affected borrowers.

Think about what that means practically. If you don’t make an active choice, here’s what happens automatically: Borrowers who do not transition plans within the 90-day period communicated by their servicer will be automatically enrolled into either the Standard Repayment Plan, or the new Tiered Standard Plan that will be available beginning July 1.

Now, here’s the critical part that I’ve seen trip up many borrowers who didn’t pay attention. If you end up in the Standard Repayment Plan by default, your monthly payments will likely be significantly higher than what you were paying under SAVE. For some borrowers, we’re talking about a jump from $0 per month to $200, $300, or even more. For someone already living paycheck to paycheck, working that Uber shift on weekends or juggling a DoorDash delivery gig to make ends meet, that sudden increase can feel impossible.

Here’s what I recommend you do right now:

Make sure your contact information is current at StudentAid.gov. This sounds simple, but the Department of Education has been clear that if they can’t reach you, your responsibility to respond doesn’t disappear. Set a reminder on your phone for early May 2026, before July 1st arrives. Check your email and mail carefully starting in June. Don’t miss that notification from your loan servicer because it will contain your specific 90-day deadline.

New Repayment Assistance Plan (RAP) vs Standard Plan: Making Your Choice

This is where things get interesting, because you have more options now than you might think.

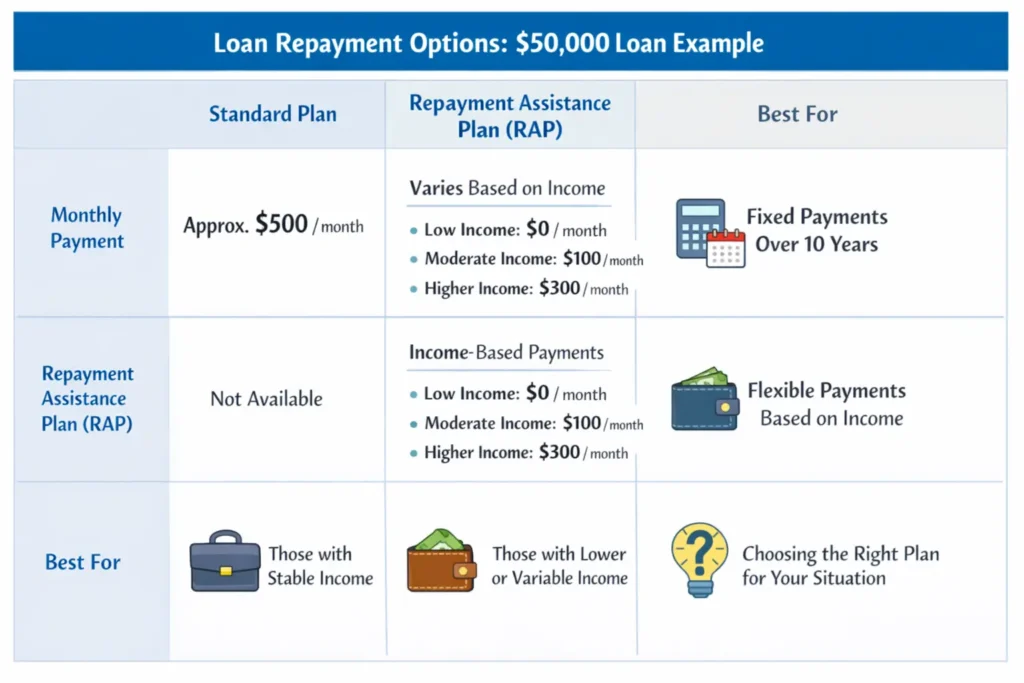

Under the OBBB, new federal loan borrowers will have just two repayment plans to choose from starting in July 2026: the standard repayment plan and the new Repayment Assistance Plan. The standard repayment plan will allow student loan borrowers to make fixed payments over the course of 10 to 25 years. The Repayment Assistance Plan will allow borrowers to pay 1% to 10% of their income on a monthly basis for up to 30 years.

Let me break down what that actually means for your wallet.

The Standard Repayment Plan (Fixed Payments)

This is the old-school approach. The new Tiered Standard Plan will offer fixed terms – 10, 15, 20, or 25 years – based on a borrower’s total outstanding loan balance, giving borrowers with higher debt lower monthly payments and more time to repay.

The benefit of this approach is predictability. You know exactly what your payment is every single month for the next 10, 15, 20, or 25 years. There’s no recalculation, no need to verify your income annually. If you love certainty and you’re confident in your income stability (maybe you have a solid 9 to 5 job at a company where you’ve been for years), this can feel comforting.

The downside? If your income fluctuates or decreases, those fixed payments don’t adjust. If you hit a rough patch financially, you can still look into deferment or forbearance, but it’s not automatic like it would be with an income-driven plan.

The Repayment Assistance Plan (RAP) – Income-Based

Under RAP, a borrower’s monthly payment is based on that borrower’s income and number of dependents. This provides borrowers with more affordable monthly payments while maintaining their repayment obligations. Unlike existing IDR plans, RAP ensures that borrowers who make full, on-time monthly payments will be shielded from runaway interest and are able to make progress toward reducing the principal balance on their loan.

Here’s why this matters for someone like you who might be working multiple gigs or whose income varies. RAP calculates your payment as a percentage of your discretionary income. Under RAP, monthly payments will typically range from 1% to 10% of your earnings; the more you make, the bigger your required payment. There will be a minimum monthly payment of $10 for all borrowers.

Think about how this plays out in real life. Your payment goes down when your income goes down. If you’re doing freelance work alongside your main job, and that side income dries up one month, your loan payment automatically becomes more affordable the following year when you recertify your income.

The tradeoff is that forgiveness takes longer under RAP (up to 30 years compared to 20-25 years under some other income-driven plans), but there’s a crucial feature: RAP includes interest subsidy protections, which means the government picks up unpaid interest to some extent if you’re paying in good faith.

Student Loan Repayment Changes July 2026: What Gets Affected Beyond Just SAVE

I want to make sure you understand the full scope of what’s changing, because it extends beyond just SAVE borrowers.

Currently, borrowers can choose from three IDR plans. However, President Trump’s One Big Beautiful Bill eliminates ICR and PAYE. After July 1, 2026, only IBR will be available.

Here’s what that means in practical terms. If you’re on Pay As You Earn (PAYE) or Income-Contingent Repayment (ICR), you won’t be able to stay on those plans indefinitely. If your loans were first disbursed on or after July 1, 2026, RAP and the new Standard Repayment Plan are your only options. You cannot enroll in Income-Based Repayment (IBR), Pay As You Earn (PAYE), Income-Contingent Repayment (ICR), or SAVE.

But here’s something important that gives me hope for existing borrowers. If your loans predate July 1, 2026, you can stay on your current plan, switch to IBR, or opt into RAP voluntarily. But PAYE, ICR, and SAVE stop accepting new enrollees on July 1, 2026, and all three sunset by July 1, 2028.

What does “sunset by July 1, 2028” mean for you? It means you have a grace period if you’re on those legacy plans. You don’t have to switch immediately, but you do need to switch before July 1, 2028. This gives you breathing room to make an informed decision, get your finances in order, and plan for the transition.

There’s also important news for Parent PLUS borrowers. Parent PLUS borrowers who have not consolidated into a Direct Consolidation Loan by June 30, 2026, permanently lose access to every income-driven repayment plan: ICR, IBR, and RAP. That also means no path to forgiveness through IDR or PSLF.

If you’re a parent who took out PLUS loans to help your child get through college, this deadline is absolutely critical. Miss it by even one day, and you lose income-driven repayment access forever. That’s not a consequence to take lightly.

The Hidden Tax Bomb: Is Student Loan Forgiveness Taxable in 2026?

Now we’re getting to something that keeps financial advisors up at night. This is the conversation that doesn’t get enough attention until it’s too late for people to prepare.

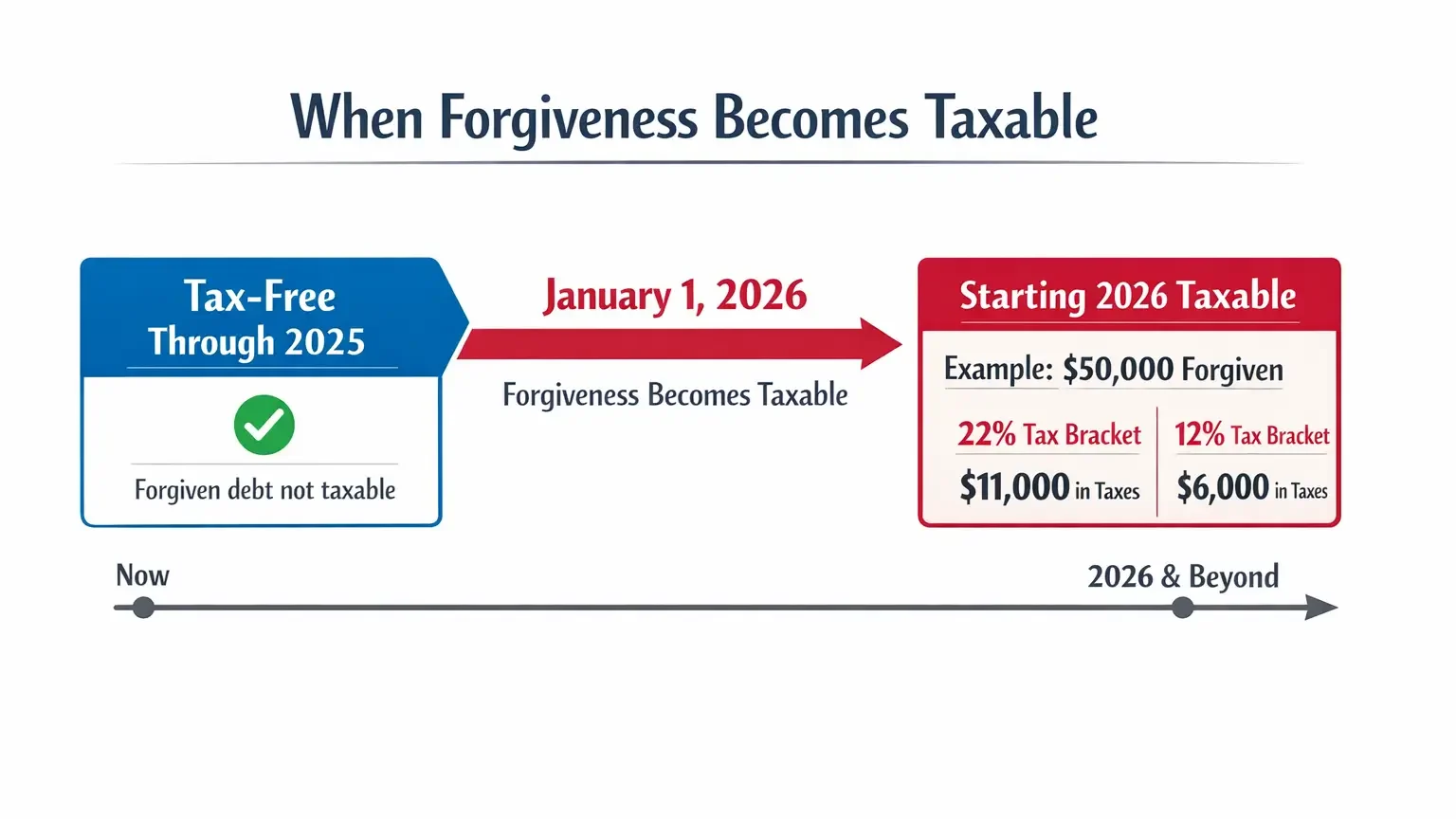

If your federal student loan balance is forgiven under an income-driven repayment plan in 2026 or later, the amount forgiven is generally treated as taxable income, known as cancellation of debt income.

Let me make sure you really understand what this means. If you’ve been on an income-driven repayment plan for 20 or 25 years, and your remaining balance of $50,000 gets forgiven in 2026, the IRS treats that $50,000 as income you received that year. You don’t receive the money in your bank account. You didn’t spend it. But the IRS looks at it as if you earned an additional $50,000 in income.

The average loan balance for borrowers enrolled in an IDR plan is around $57,000. For those in the 22% tax bracket, having that amount forgiven would trigger a tax burden of more than $12,000.

Let that sink in for a moment. You’ve finally made it to the forgiveness finish line after decades of payments, and suddenly you’re facing a tax bill that could exceed $12,000. For a lower-income borrower in the 12% tax bracket with $57,000 forgiven, the bill could still be around $7,000.

The good news is that there’s a grace period built into the rules for some people. Borrowers who became eligible for student loan forgiveness in 2025 won’t owe federal taxes on the relief, even if their debt isn’t officially discharged until later. That means if you received confirmation in 2025 that you’re eligible for debt cancellation, you should save that dated record.

But if you become eligible for forgiveness starting in 2026, you will owe taxes on the forgiven amount unless Congress changes the law.

There is one important exception.

These tax changes do not impact forgiveness under the Public Service Loan Forgiveness (PSLF) program, which is not considered taxable income. If you’re a teacher, nurse, government worker, or nonprofit employee pursuing PSLF, your forgiveness remains tax-free. That’s one reason why PSLF has become so valuable to borrowers in these professions.

How to Switch Student Loan Plans Before July Deadline

Now that you understand your options, let’s talk about the actual mechanics of switching plans. This is where clarity really helps.

Step 1: Know What Plan You’re Currently On

Log into StudentAid.gov and look up your current repayment plan. Write it down or take a screenshot. This seems obvious, but I’ve seen borrowers struggle because they weren’t sure which plan they were actually on, especially if they’d moved servicers over the years.

Step 2: Use the Federal Loan Simulator Tool

The Department of Education has a tool specifically designed for this moment. Borrowers can use the federal Loan Simulator tool to estimate their payments and view loan options.

This tool lets you plug in your income, family size, and loan balance, and it calculates what your payments would be under different plans. It’s free, it’s online, and it removes the guesswork. Spend 15 minutes with this tool. It could save you thousands of dollars over the life of your loan.

Step 3: Consider Your Personal Situation

Ask yourself these questions:

Is your income stable or does it fluctuate? If you’re doing gig work (Uber, DoorDash, freelancing), an income-based plan like RAP makes more sense. If you have a stable 9-to-5 job, the Standard Plan’s predictability might appeal to you.

How much longer can you keep making payments? If you’re close to forgiveness under an income-driven plan, tax planning becomes crucial. If you’re just starting, you have more time to make your choice and adjust later if needed.

Are you pursuing Public Service Loan Forgiveness? If yes, you must stay on an income-driven plan. IBR is your reliable option.

Step 4: Submit Your Application Early

The Education Department is working through a backlog of income-driven repayment plan applications, with more than 576,000 requests pending as of the end of February.

This is critical. There’s already a backlog of half a million applications sitting in the system. If you wait until August to submit your plan change, you could be waiting months for it to be processed. Apply early in the summer, even in May if you can. Don’t assume the system will process your request quickly.

Step 5: Verify Your Employment (If Pursuing PSLF)

Certify your employment and confirm your qualifying payment count before July 1. Payments credited under the current employer eligibility rules are not affected by the new “substantial illegal purpose” standard.

If you’re pursuing loan forgiveness through PSLF, log into StudentAid.gov and verify that your employer information is correct and that your payment count is accurate. Don’t let errors sit there and compound over time.

Real-Life Scenarios: How People Like You Are Preparing

Let me show you how this plays out in actual lives, because understanding the theory is one thing, but seeing it in practice is where it clicks.

Scenario 1: Marcus, a DoorDash Driver with Variable Income

Marcus is 34 and has been doing DoorDash delivery combined with part-time retail work for three years. His student loan balance is $48,000, and he’s been on SAVE paying based on his income. Some months he makes $2,000; other months, during the winter, he only makes $1,200. Under SAVE, his payments adjusted year to year, and some months he qualified for just $50 or $75 monthly payments.

When Marcus looked at the Standard Plan, his payment would be about $550 per month for the next 15 years. That would require him to cut his delivery gigs or retail shifts, which isn’t realistic.

Instead, Marcus chose to transition to RAP when it becomes available July 1st. His payments will still be based on his actual monthly income, and he’ll have the flexibility he needs while making real progress on his principal balance. Yes, his forgiveness timeline extends to 30 years instead of his original timeline, but with variable income, RAP is his path forward.

Scenario 2: Jennifer, a Teacher Pursuing Public Service Loan Forgiveness

Jennifer teaches elementary school and carries $65,000 in student loans. She’s been on SAVE but has been making regular payments toward Public Service Loan Forgiveness. She has about 6 years until she hits her 120 qualifying payments.

Jennifer’s situation is straightforward. She must move to an income-driven plan before her SAVE plan ends, and Income-Based Repayment is her best choice because it keeps her on an eligible path for PSLF. Her monthly payment will increase slightly compared to SAVE (from about $280 to $350), but her path to tax-free forgiveness through PSLF remains intact. After her 120 qualifying payments are made, she’ll have $45,000 forgiven tax-free, which makes it worth the wait.

Scenario 3: David, a Professional with Stable Income Nearing Forgiveness

David is a 52-year-old accountant earning $85,000 per year with a fairly stable income. He’s been in an income-driven repayment plan for 22 years and is approaching the finish line. He has about $38,000 left to be forgiven.

Here’s David’s dilemma: his forgiveness is coming in 2027, which means it will be taxable. He started saving 24 months ago, putting aside $1,500 per month into a dedicated savings account specifically for his eventual tax bill. When his $38,000 is forgiven, he’ll face roughly $8,000-$9,000 in federal taxes, but he’ll have the money set aside to handle it. His peace of mind about this potential tax bill has been worth more than the interest he might have earned in a savings account.

Your Action Plan: Starting Today

You don’t have months to figure this out. You have weeks. Let me give you a specific action plan that you can start executing today.

This Week:

- Log into StudentAid.gov and verify your current repayment plan and your contact information.

- Make sure you have a current email address and phone number on file with your loan servicer. (You can find your servicer’s information on StudentAid.gov as well.)

- Check if you have any applications that are pending from previous requests.

By the End of May 2026:

- Use the Federal Loan Simulator tool to model out your two best options.

- If you’re a Parent PLUS borrower, start the consolidation application immediately. Don’t wait.

- Write down your specific 90-day deadline once you receive your servicer’s notice.

By June 30, 2026:

- Have submitted your repayment plan change application.

- Verify it was received by your servicer.

- If you’re pursuing PSLF, confirm your employment certification is current.

Starting July 1, 2026:

- Watch for notifications from your servicer about your plan transition.

- Confirm which plan you’ve been enrolled in.

- If automatic enrollment occurred and you don’t like your assigned plan, you can change it. You’re not locked in.

Why This Matters Beyond Just Your Student Loans

I want to step back for a moment and acknowledge something deeper here. Your student loans aren’t just a financial obligation. For many of you, they’re connected to your biggest life dreams. Someone used that money to pursue an education that was supposed to open doors. The fact that those doors often came with a financial burden attached is a separate conversation, but the promise was real.

The changes coming in July 2026 aren’t happening to you to make your life harder. They’re policy shifts driven by larger political and economic conversations. But you still have agency here. You have the ability to understand your options, make an informed choice, and position yourself in the way that works best for your life.

This is exactly the kind of financial challenge where preparation pays off. The difference between someone who ignores this deadline and someone who actively chooses their path forward could be thousands of dollars in monthly payments over the life of their loan.

FAQs About July 2026 Student Loan Changes

What happens if I don’t choose a new repayment plan by my 90-day deadline?

You’ll be automatically enrolled in either the Standard Repayment Plan or the new Tiered Standard Plan. For most borrowers, this will result in significantly higher monthly payments than they were paying under SAVE. You can still change plans after automatic enrollment, but you should actively choose rather than default.

Can I stay on my current plan if it’s not SAVE?

It depends on your plan. If you’re on Income-Based Repayment (IBR), you can stay indefinitely. If you’re on SAVE, PAYE, or ICR, you can stay until July 1, 2028, but you cannot enroll in a new legacy plan after July 1, 2026. So you have breathing room, but you need a plan before 2028.

Is switching repayment plans going to reset my progress toward loan forgiveness?

In most cases, no. Switching plans does not reset your progress toward PSLF or IDR forgiveness in most cases. Your qualifying payment count carries over. This is important because it means your years of payments count toward forgiveness under your new plan.

What’s the difference between the old income-driven plans and RAP?

RAP is newer and includes some protections that older plans don’t. Unlike existing IDR plans, RAP ensures that borrowers who make full, on-time monthly payments will be shielded from runaway interest and are able to make progress toward reducing the principal balance on their loan. This means interest doesn’t pile up as easily if you’re making good-faith payments.

Will my taxes really change if my student loans are forgiven?

Yes, for most borrowers in income-driven repayment plans. Starting January 1, 2026, many types of loan forgiveness will automatically become taxable again unless Congress extends the exemption. The exception is Public Service Loan Forgiveness, which remains tax-free. If you’re expecting forgiveness in the coming years, this should factor into your financial planning.

Do I lose access to deferment and forbearance options?

The rules are changing here too. New federal student loans will no longer be eligible for economic hardship or unemployment deferments, which let you pause payments when you couldn’t afford them. This applies to loans issued on or after July 1, 2027. This affects new borrowers more than existing borrowers, but it’s worth knowing if you take out more loans in the future.

What should I do if I’m on the SAVE plan but also pursuing Public Service Loan Forgiveness?

Switch to an income-driven plan that continues to qualify for PSLF, which is Income-Based Repayment (IBR). Your payments will likely be slightly higher than SAVE, but your path to tax-free forgiveness through PSLF is protected. This is the secure choice for you.

Where can I get help understanding these changes?

The Federal Student Aid office has information at StudentAid.gov. You can also contact your loan servicer directly. Some nonprofits like TISLA (Institute of Student Loan Advisors) offer free guidance. Don’t pay for advice on choosing a standard repayment plan unless you want help with complex tax planning for forgiveness.

Moving Forward With Confidence

You started reading this article feeling uncertain about what July 2026 brings. I hope you’re finishing it with a clearer picture and a sense of what you need to do. The July 2026 student loan changes are real, they’re coming, and they’ll affect millions of Americans. But they’re not a disaster waiting to happen. They’re a transition that requires thoughtfulness and preparation.

Start with StudentAid.gov. Use the Loan Simulator. Look at your personal situation honestly. Make an active choice about your repayment plan instead of letting the system make one for you. Understand the tax implications if forgiveness is in your future. And if you’re a Parent PLUS borrower, don’t procrastinate on consolidation—that June 30, 2026 deadline is absolute.

I’ve watched people successfully navigate changes like these. They didn’t ignore the deadline. They didn’t assume everything would work out. They sat down, did a little homework, and made informed decisions. You can do the same.

Your financial future is worth a few hours of research. I have strong confidence that you’ll make the right choice for your situation.

Disclaimer: This article is for educational and informational purposes only. It is not financial, investment, or legal advice. Always consult a qualified financial advisor before making any financial decisions.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.

2 thoughts on “Don’t Wait for July 2026! 7 Critical Student Loan Steps You Must Take Before the SAVE Plan Ends”