Why Your Emergency Fund Is Your Greatest Financial Shield

I’m going to be honest with you right from the start. An emergency fund isn’t glamorous. It’s not exciting to talk about. But it’s the single most important financial decision you’ll make this year.

Think about what happens when your car breaks down and you have no savings. Or your hours get cut at work. Or a medical bill lands in your mailbox. Without an emergency fund, you reach for a credit card. And suddenly you’re drowning in debt that takes years to escape.

I’ve talked to thousands of people struggling with debt, and almost every single one says the same thing: “I wish I’d had emergency savings before everything fell apart.”

Here’s the truth I’ve learned: an emergency fund isn’t about being pessimistic. It’s about being realistic. Life happens. Cars break down. Job markets shift. Medical emergencies occur. This isn’t a question of if something unexpected will happen. It’s when.

The good news? Building an emergency fund doesn’t require winning the lottery or getting a promotion. It requires intention and action. And that’s exactly what side hustle ideas for building emergency funds are all about.

An emergency fund typically means three to six months of living expenses set aside. For most people, that’s $3,000 to $10,000. That sounds like a lot until you break it into smaller goals. Save $1,000 first. Then $2,500. Then build from there.

This is where side hustles change everything. A side hustle isn’t about getting rich quick. It’s about creating a second income stream that flows directly into your financial security. Every dollar from your side gig can go straight into your emergency fund instead of feeding lifestyle inflation.

The Side Hustle Reality: What Actually Works in 2026

Before I show you specific side hustle ideas for building emergency funds, let me be real about what works and what doesn’t in 2026.

The side hustle landscape has changed dramatically in the last two years. Some things that promised easy money in 2024 are harder now. But other opportunities have opened up. The key is understanding what’s actually realistic.

Here’s what I’ve learned works:

Low Barrier to Entry: The best side hustles don’t require thousands of dollars upfront. They require your time and effort, not your capital.

Flexible Timing: Your main job owns most of your day. Your side hustle needs to fit around that reality, not replace it immediately.

Real Income: This isn’t about making $5 per month. We’re talking side hustles that can generate $300 to $1,500+ monthly, depending on effort and time investment.

Scalable: As you get better and more efficient, income should increase. You shouldn’t be maxed out after two weeks.

Legitimate: No pyramid schemes, no “work from home make $10,000/week” scams, no get-rich-quick garbage. Just real work that pays real money.

The side hustle ideas I’m about to share all meet these criteria. Some are gig economy based. Some rely on your skills. Some are semi-passive once they’re established. All of them can contribute meaningfully to your emergency fund goal.

10 Side Hustle Ideas for Building Emergency Funds That Fit Your Life

Let me walk you through the side hustle ideas that real people are using right now to build their emergency funds. I’ve grouped them by type so you can find what fits your situation best.

Idea 1: Delivery and Rideshare (Gig Economy)

This is the most accessible entry point for most people. If you have a car that’s reliable and good insurance, you can start earning within days.

The Real Numbers:

Uber drivers report making $15 to $25 per hour on average, depending on location and time. DoorDash drivers typically make $15 to $23 per hour. Some nights are better than others.

Here’s the catch: You’re not making $20 per hour. You’re making $20 per hour minus vehicle wear and tear, gas, insurance increases, and taxes. A realistic take-home is $12 to $18 per hour.

But that’s still legitimate income. Working 15 to 20 hours per week at DoorDash could mean $200 to $350 per week, or $800 to $1,400 monthly. For an emergency fund, that’s huge progress.

Best For:

People with flexible schedules. People who already have a reliable car. People who want immediate income (not waiting weeks for first payment).

Time to First Payment: 1 to 2 weeks

Startup Costs: None (you already have the car)

Realistic Monthly Income: $800 to $1,500

Idea 2: Freelance Writing and Content Creation

If you can write clearly, the internet has endless demand for your words. Companies need blog posts, product descriptions, email copy, social media content, and more. They’re willing to pay for it.

Where to Find Work:

Platforms like Fiverr, Upwork, Contently, and WriterAccess connect writers with clients. You can also pitch directly to websites and blogs that publish content in your area of expertise.

Starting rates for new writers are $20 to $50 per article or per 1,000 words. Experienced writers charge $100 to $300+. You can absolutely work your way up.

Best For:

People who enjoy writing. People who have knowledge or expertise in a specific area (health, finance, technology, parenting, etc.). People who want to work from home with zero startup costs.

Time to First Payment: 2 to 4 weeks (depends on finding first client)

Startup Costs: None

Realistic Monthly Income: $500 to $2,000+ (depending on output and rates)

Idea 3: Virtual Assistance

Busy entrepreneurs, small business owners, and coaches need help with emails, scheduling, data entry, customer service, and administrative tasks. They’ll pay someone to handle this.

Virtual assistant work typically pays $15 to $25 per hour to start, scaling up to $25 to $50+ as you gain experience and take on more complex tasks.

You might help manage calendars, respond to emails, schedule social media posts, handle customer inquiries, or organize files. The work is repetitive but straightforward.

Best For:

Organized people who are detail-oriented. People who enjoy helping others organize their business. People who prefer clear structure and defined tasks over creative work.

Time to First Payment: 3 to 6 weeks (finding clients takes time)

Startup Costs: None to minimal

Realistic Monthly Income: $600 to $1,800

Idea 4: Social Media Management

Every small business needs social media presence, but most business owners hate managing it. This is where you come in.

You manage their Instagram, TikTok, Facebook, or LinkedIn. You create content calendars, post content, respond to comments, and grow their audience. Small businesses typically pay $300 to $1,000 monthly for a social media manager.

You might manage 3 to 5 clients, each paying $300 to $500 monthly. That’s $900 to $2,500 per month in pure income.

Best For:

People who are comfortable on social media. People who understand content trends and engagement. People who are organized and can manage multiple client accounts. Ideally, people with a portfolio showing past success.

Time to First Payment: 4 to 8 weeks (building portfolio and finding clients)

Startup Costs: None to minimal

Realistic Monthly Income: $900 to $2,500

Idea 5: Pet Sitting and Dog Walking

This is one of the most underrated side hustles. Pet owners love their animals and will pay good money for someone trustworthy to care for them.

Apps like Rover and Care.com connect pet sitters with clients. A 30-minute dog walk might pay $15 to $25. A full day of pet sitting could pay $50 to $100. Some pet sitters charge flat rates for overnight stays or extended periods.

A pet sitter managing 5 to 10 walks per week could make $300 to $600 monthly. More if you pick up additional clients or overnight sits.

Best For:

People who love animals. People in areas with lots of pet owners (suburbs, urban areas). People who have flexible timing during the day. People who don’t mind physical activity.

Time to First Payment: 1 to 2 weeks (apps process quickly)

Startup Costs: None

Realistic Monthly Income: $300 to $900

Idea 6: Online Tutoring and Teaching

If you have knowledge in a specific subject, you can teach it online. Math, English, languages, test prep, music lessons, coding, professional skills. The demand is huge.

Platforms like Tutor.com, Chegg, Wyzant, and Care.com connect tutors with students. Rates typically range from $15 to $60 per hour depending on subject and your qualifications. Some tutors charge more.

Teaching 5 to 10 hours per week at $25 per hour means $125 to $250 weekly, or $500 to $1,000 monthly.

Best For:

Teachers or people with professional expertise. People who enjoy explaining complex ideas simply. People with teaching credentials or advanced degrees. People who want flexible scheduling.

Time to First Payment: 2 to 4 weeks

Startup Costs: None to minimal (possibly good lighting and microphone)

Realistic Monthly Income: $500 to $1,500

Idea 7: Freelance Graphic Design and Visual Content

If you can design, there’s massive demand. Logos, social media graphics, presentation decks, infographics, book covers, website designs. Businesses need this stuff constantly.

Even if you’re not classically trained, tools like Canva make it accessible. You can create professional-looking designs with templates and sell them.

Graphic designers on Fiverr charge $50 to $300+ per project. Some charge hourly ($25 to $100+). You might complete 2 to 5 projects weekly, depending on complexity.

Best For:

People with design skills or who are willing to learn design tools. People who are creative and detail-oriented. People who want project-based work instead of hourly.

Time to First Payment: 3 to 6 weeks (building portfolio)

Startup Costs: $10 to $20/month for Canva Pro or design software

Realistic Monthly Income: $600 to $2,500

Idea 8: Selling Products Online (Dropshipping, Print-on-Demand)

This is semi-passive once set up. You create an online store, upload designs or products, and customers order them. Companies like Printful, Teespring, and Shopify handle fulfillment and shipping.

You make a profit on the difference between production cost and selling price. A t-shirt might cost $5 to produce and sell for $20. That’s a $15 profit per shirt.

This requires marketing to drive traffic, but once you have a store running, income can come in relatively passively.

Best For:

People interested in design or finding market niches. People willing to invest time in marketing and social media. People who want semi-passive income. People who are patient (this builds slowly).

Time to First Payment: 4 to 12 weeks

Startup Costs: $20 to $100 (platform fees, maybe some marketing)

Realistic Monthly Income: $200 to $1,500 (after initial ramp-up)

Idea 9: Freelance Proofreading and Editing

Writers, students, and business professionals need editing help. You read their work, catch errors, improve clarity, and ensure consistency. They pay you for this service.

This requires attention to detail but not necessarily extensive training. Many people pick up proofreading through practice.

Rates vary from $20 to $75+ per hour depending on document type and your experience. A proofreader might complete 3 to 8 projects weekly.

Best For:

People with excellent grammar and attention to detail. People who enjoy reading and improving written work. People who are organized and methodical. People who don’t mind repetitive work.

Time to First Payment: 3 to 6 weeks

Startup Costs: None to minimal

Realistic Monthly Income: $400 to $1,200

Idea 10: Handmade Crafts and Digital Products

If you make things, people will buy them. Etsy is the obvious platform. You might sell handmade jewelry, art, home décor, vintage items, or digital products (templates, planners, graphics).

Digital products are especially interesting because once created, they’re pure profit. Create an Excel budget template, sell it for $5, and you make that profit on each sale.

Some Etsy sellers make $100 monthly from their shop. Others make $5,000+. It depends on product quality, niche, and marketing effort.

Best For:

Creative people with a specific skill or talent. People who like making things. People interested in building a long-term business. People willing to invest in marketing.

Time to First Payment: 2 to 4 weeks (setting up shop)

Startup Costs: $20 to $200 (depending on materials and platform fees)

Realistic Monthly Income: $100 to $2,000

Also read:- What Is an Average Credit Score in 2026? 7 Secrets Your Bank Doesn’t Want You to Know

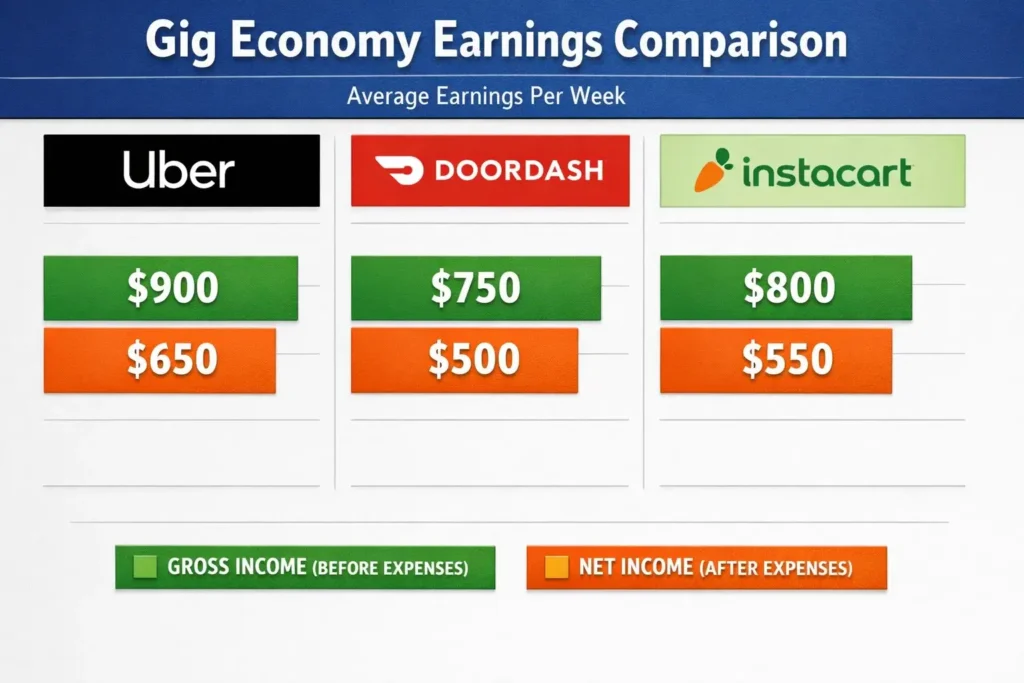

The Gig Economy Giants: Uber, DoorDash, and Beyond

Let me spend a moment on gig economy platforms because they’re the most accessible starting point for most people wanting to build an emergency fund quickly.

Why Gig Economy Works for Emergency Funds:

You get paid frequently (often weekly). You control your own schedule. You don’t need anyone’s permission or approval. You can start immediately. There’s immediate money available.

The Honest Truth About Gig Work:

Your car is your biggest asset and your biggest cost. Gas, maintenance, insurance, and depreciation matter. A lot. Work during peak hours (evenings and weekends) for better pay. Early morning or random hours pay less.

Weather affects everything. Rain increases delivery demand but makes driving harder. Snow can shut everything down. Holidays are chaotic but often high-earning.

Customer ratings matter. A few bad ratings can hurt your ability to get good orders. You need to be reliable, professional, and responsive.

Gig Economy Reality Check:

If you drive for DoorDash for 12 hours per week at realistic take-home rate of $15/hour, that’s $180 weekly or about $720 monthly. That’s enough to build a small emergency fund over several months.

If you add Uber and DoorDash, doing 20 hours per week combined, you could legitimately make $1,200 to $1,500 monthly.

This isn’t getting rich. But it’s getting safe. And that’s worth everything.

Creative and Skill-Based Side Hustles for Real Income

If gig economy work doesn’t appeal to you, skill-based side hustles offer better long-term income potential. The catch is they take longer to establish.

Why Skill-Based Hustles Work Better Long-Term:

As you get better and develop a reputation, rates increase. You’re not stuck at the same price forever. You can specialize and charge premium rates.

Your income isn’t limited by hours in a day. A freelance designer can scale to multiple clients. A tutor can teach groups. A writer can create once and sell multiple times.

You build assets (a portfolio, client relationships, reputation) that generate value even when you’re not actively working.

The Timeline Reality:

Months 1 to 2: You’re learning, building portfolio, finding first clients. Income is minimal.

Months 3 to 6: You’re getting more clients, rates are improving, income becomes consistent.

Months 6 to 12: You’ve got reviews, testimonials, and a reputation. You can be selective about clients and charge more.

Year 2+: You’ve got steady income, repeat clients, and potentially premium rates.

This is why many people combine gig work (immediate income) with skill-based work (building long-term income).

For example, work DoorDash 10 hours weekly for immediate $500 to $700. Spend another 10 hours weekly on freelance writing to build that income from $200 to $500 to $1,000. Within 6 months, you’ve shifted from heavy gig work to better-paying creative work, and your emergency fund is growing faster.

Passive and Semi-Passive Income Streams

Real talk: truly passive income is rare. But semi-passive income exists, and it can contribute meaningfully to your emergency fund over time.

What Makes Income Semi-Passive?

You do work upfront. You create the thing once. Then it generates income repeatedly with minimal maintenance.

Examples of Semi-Passive Income:

Digital products (templates, courses, ebooks) that you create once and sell indefinitely. You do the work once. The platform handles fulfillment. You collect profit.

Affiliate marketing (recommending products or services you use and getting commission). You write one article. Readers click your link. You earn commission from sales. It’s passive except for the initial writing.

Stock photography (selling photos you’ve already taken). You upload images to Shutterstock or iStock. People license them. You collect royalties monthly.

Content creation (YouTube, podcasting, blogging) that eventually generates sponsorship or ad revenue. This requires months or years of consistent work before income materializes.

Rental income (renting out a parking space, room, equipment). You own something, someone pays to use it.

Why Semi-Passive Matters:

If you build one semi-passive income stream earning $200 monthly, that’s $2,400 yearly toward your emergency fund. You’re not actively trading hours for dollars anymore. You’re collecting recurring revenue.

The catch? Building semi-passive income takes patience. You typically don’t make real money for 3 to 6 months. But once you do, the income comes in while you’re sleeping, working your day job, or pursuing other hustles.

Building Your Emergency Fund Strategy: The Action Plan

Okay, you know the side hustle ideas. Now let’s talk strategy. Because knowing about side hustles and actually building an emergency fund are two different things.

Step 1: Calculate Your Emergency Fund Target

How much do you actually need? This isn’t an abstract number.

Write down your monthly expenses. Everything: rent, utilities, food, insurance, transportation, debt payments. Add them up.

That’s your monthly burn rate.

For a true emergency fund, multiply that by 3 to 6 months. That’s your target. For many people, that’s $3,000 to $10,000.

But you don’t need that all at once. Start with a $1,000 starter emergency fund. Then build to $2,500. Then three months of expenses. Break it into achievable milestones.

Step 2: Choose Your Side Hustle(s)

Not one side hustle is perfect. Different hustles serve different purposes.

Choose one that has low barrier to entry (gig work like DoorDash) and one with long-term income potential (freelance writing or virtual assistance). Combine them strategically.

Month 1 to 3: Do gig work 15 to 20 hours weekly for immediate income. Start building skill-based side hustle 5 to 10 hours weekly.

Month 3 to 6: As skill-based income grows, slightly reduce gig work. Shift time toward what’s earning better.

Month 6+: You’ve got multiple income streams. One is providing base emergency fund building. One is growing in income potential.

Step 3: Automate Your Savings

This is the most important part. Every single dollar from your side hustle must go to your emergency fund. Not to wants. Not to lifestyle improvements. To your fund.

Set up automatic transfers. When you get paid from DoorDash, transfer 70% to your emergency fund. When you get paid from freelance work, same thing. Make it automatic so you don’t have to think about it.

This is how you avoid side hustle income disappearing into your regular budget.

Step 4: Track Your Progress

Create a simple spreadsheet showing your starting point and your target. Update it monthly.

Seeing progress is motivating. When you go from $0 to $500 to $1,200 to $2,500, you feel the momentum. Don’t underestimate the power of this.

Step 5: Stay Consistent

Side hustles don’t work if you do them inconsistently. Commit to a schedule. Monday and Thursday nights you do DoorDash. Tuesdays and Saturdays you do freelance work. Make it a habit.

Consistency compounds. Four weeks of 15 hours produces a certain amount. But 12 weeks of consistent 15 hours produces momentum that builds on itself.

Real Stories: How Others Built Their Security Net

Story 1: Jennifer’s Food Delivery to Freelance Transition

Jennifer was a 28-year-old administrative assistant making $38,000 yearly. Her job was stable but not enough. She had no emergency fund. One car repair bill would destroy her.

In January 2025, she started DoorDash two evenings per week. She made $400 to $500 monthly. Not huge, but it was money she’d never had.

She also started writing blog posts on Upwork. Her first month: one client, $150. Month two: two clients, $400. Month three: three clients, $900.

By June 2025, her DoorDash income was still $450 monthly, but her freelance writing had grown to $1,200 monthly. Total side income: $1,650.

She kept this pattern through 2025. By December 2025, she had built a $5,000 emergency fund. More importantly, she’d shifted from gig work to skill-based work that paid better and felt more sustainable.

In 2026, her freelance writing is at $1,800 monthly (scaling rates as experience grew). She’s reduced DoorDash to occasional weekend work just to keep it as backup. Total side income: $2,000 to $2,500 monthly.

Her emergency fund is now $8,000. Her day job covers everything. Her side income builds wealth.

Story 2: Marcus’s Gig Stack Approach

Marcus was a 32-year-old teacher making decent money but with no emergency savings. He had student loans and a car payment. He needed security.

He combined three gig opportunities: Uber 8 hours weekly, DoorDash 8 hours weekly, and TaskRabbit 4 hours weekly (doing odd jobs).

At realistic rates: Uber: 8 hours at $16/hr net = $128 DoorDash: 8 hours at $15/hr net = $120 TaskRabbit: 4 hours at $18/hr = $72

Total per week: roughly $320 Total per month: roughly $1,280

It wasn’t glamorous. But every month for 12 months, $1,280 went straight to his emergency fund.

By December 2025, Marcus had $15,000 in emergency savings. He maintained this through all of 2026. He’s not getting rich, but he’s completely safe. His teaching job covers expenses. His side income is pure security.

Story 3: Priya’s Digital Product Pivot

Priya was a 26-year-old graphic designer with freelance design work paying inconsistently ($500 to $1,500 monthly depending on projects).

In early 2025, she started creating digital products: Canva templates for social media posts, email newsletter templates, and presentation templates. She sold them on Etsy for $5 to $15 each.

Month 1: 3 sales, $25 revenue Month 2: 8 sales, $68 revenue Month 3: 25 sales, $200 revenue

She reinvested some profits into marketing. By month 6, she was making $400 to $600 monthly from digital products. Combined with freelance design work, her total income was $1,000 to $2,000 monthly.

The beauty? Her digital product income grew to $800+ monthly by December 2025. That’s nearly pure profit (minimal costs after initial creation). It’s semi-passive. It keeps earning while she sleeps.

Her emergency fund grew to $6,000 by end of 2025. In 2026, it’s growing faster because digital product revenue is more stable and scalable than project-based freelance work.

What These Stories Show:

Emergency funds aren’t built overnight. They’re built month by month through consistent side hustle effort. Different approaches work for different people. Some people thrive with gig stacks. Others prefer developing skill-based income. Most people do a combination.

The common thread? Consistent action + automatic savings = emergency fund.

Avoiding Side Hustle Burnout While Building Your Fund

Here’s something nobody talks about: side hustles can destroy you if you’re not careful.

Working your 9 to 5, then coming home to do DoorDash until 9 PM, then trying to squeeze in freelance work on weekends. That’s 12 to 14 hours daily. That’s not sustainable.

People burn out. They quit. They never build their emergency fund.

How to Avoid the Burnout Trap:

- Set realistic hours. Commit to 15 to 20 hours weekly of side work. Not 40. Not 50. Fifteen to twenty. That’s achievable alongside a full-time job.

- Take one full day off per week. No side hustles. Just rest. Your brain and body need recovery.

- Rotate your side hustles. Don’t do the same thing every day. Mix gig work with creative work. The variety keeps your brain engaged instead of fried.

- Have a clear timeline. “I’m doing this heavy side hustle phase for six months until I have $3,000 saved.” Knowing there’s an endpoint matters psychologically.

- As your emergency fund grows and side income improves, pull back. You don’t need to maintain high hours once you’ve got security. Maintain enough to keep the momentum but not so much that you burn out.

The Better Approach:

- Month 1 to 3: High effort (20 hours weekly). Build momentum and get quick wins.

- Month 3 to 6: Moderate effort (15 hours weekly). You’ve got some savings now. You know what works. Optimize rather than maximize.

- Month 6 to 12: Maintenance effort (10 to 15 hours weekly). Your emergency fund is substantial. You’re preventing burnout while still building.

- Year 2: Selective effort. Do only the side hustles you enjoy. Let your favorite income stream grow while others sit.

This is how side hustles become sustainable instead of soul-crushing.

The Psychology of Building Emergency Funds

Building an emergency fund through side hustles requires more than just hard work. It requires emotional resilience.

Why Emergency Funds Are Psychologically Hard:

You’re adding work to your already full life. You’re delaying gratification. You’re saying no to social activities and fun. Your friends are going out on Friday night. You’re driving for DoorDash instead.

It feels self-punishing in the moment. But it’s actually self-loving. You’re paying future-you in security and peace of mind.

Making It Emotionally Sustainable:

Every time you add money to your emergency fund, celebrate it. Not with spending. With acknowledgment. “I just added $200 to my security. I’m getting safer.”

Tell people what you’re doing. Having accountability helps. Tell your partner, your best friend, your family. “I’m building my emergency fund.” Now they know what you’re doing and can support instead of question.

Picture what that emergency fund means. It means your car breaking down isn’t a financial crisis. It means losing your job isn’t a panic situation. It means unexpected illness doesn’t mean debt. Hold onto that vision.

Measure progress not just in dollars but in freedom. At $1,000, you have one month of breathing room. At $3,000, you have real security. At $6,000, you have options.

This isn’t about suffering. It’s about building the foundation for actually enjoying your life without financial terror in the background.

FAQs About Side Hustles and Emergency Funds

Q: What’s the fastest side hustle to start earning money?

A: Gig work like DoorDash or Uber. You can apply, get approved, and start earning within days. First payment comes within 1 to 2 weeks. It’s not the highest-paying option long-term, but it’s the fastest to actual income.

Q: Can I really build a meaningful emergency fund on side hustle income alone?

A: Absolutely, but it takes time and consistency. If you earn $1,000 monthly from side hustles, you’ll have $3,000 saved in three months, $6,000 in six months. That’s real money. Most people can eventually replace an emergency fund and then some with consistent side work.

Q: How much should I keep in my emergency fund before I shift focus to paying off debt?

A: Get to at least $1,000 first. That breaks the debt cycle. Then tackle high-interest debt (credit cards, personal loans) while maintaining your emergency fund. Once debt is gone, rapidly expand the fund to 3 to 6 months of expenses. You can’t build real wealth while drowning in high-interest debt.

Q: Is it better to do one side hustle or multiple?

A: One focused hustle works better than scattered effort across five. Pick one main side hustle where you’re really committed. If you want multiple, do one that’s immediate income (gig work) and one that builds long-term income (freelancing). But don’t spread yourself across five different platforms trying to do everything.

Q: What if I don’t have a skill for freelance work?

A: Start with gig work. But also start building a skill. Learn writing from YouTube and practice. Take a virtual assistant course on Udemy for $10. Learn graphic design basics through Canva. In 3 to 6 months, you’ll have enough competency to start freelancing. Meanwhile, gig work builds your fund immediately.

Q: How long should I maintain my side hustle after building the emergency fund?

A: Don’t stop. Shift focus. Your emergency fund is your floor, not your ceiling. Keep earning on the side, but instead of 20 hours weekly, maybe do 8 to 10 hours. Put that income toward paying off debt, building wealth, or investing. A side hustle becomes part of your financial structure.

Q: Am I supposed to pay taxes on side hustle income?

A: Yes. Side hustle income is taxable. You’ll need to track expenses and either pay quarterly estimated taxes or pay it all at tax time. Talk to a tax professional. This is important. The worst case is making good money and then owing a huge tax bill you didn’t plan for.

Q: What if I start a side hustle and hate it?

A: Switch. If DoorDash is destroying your motivation, stop and try virtual assistance. If freelance writing isn’t working, try pet sitting. The side hustle that works is the one you’ll actually do consistently. It doesn’t have to be your passion, but it can’t be something you actively hate.

The Relationship Between Emergency Funds and Debt Payoff

I want to address something important that doesn’t get talked about enough. How do emergency funds and debt payoff connect?

The Vicious Cycle Without Emergency Savings:

You have credit card debt. You don’t have emergency savings. Your car breaks down. You can’t afford to fix it, so you put it on another credit card. Now you have more debt. A medical bill comes. Another card. You’re in a hole digging deeper.

This is why people with side hustle income need to strategically build an emergency fund first.

The Better Strategy:

Month 1 to 2: Build a small emergency fund ($1,000). This is your financial airbag.

Month 3 onward: Split your side hustle income. 50% to emergency fund (building to 3 to 6 months expenses). 50% to debt payoff.

Once you have adequate emergency savings, shift to 100% debt payoff while maintaining minimum emergency fund contributions.

Once debt is gone, shift all side hustle income to building wealth instead of survival.

This is why side hustles matter so much. They give you the breathing room to build safety AND attack debt simultaneously. Without side income, you’re trapped choosing between emergency fund and debt payoff.

For more strategic debt management, check out [Credit Card Payoff Plans] to see how aggressive payoff strategies work when you have side income flowing in.

The 2026 Side Hustle Landscape

The side hustle world in 2026 is different than it was in 2024. Some things have gotten harder. Some have gotten easier.

What’s Changed:

Gig economy competition is fierce in saturated markets. In major cities, making $20/hour from DoorDash is harder than it was two years ago. But in suburban and rural areas, rates are actually higher due to less competition.

Freelance rates have stabilized. The race to the bottom (where everyone charges $5 per article) has ended. Quality freelancers are commanding $30 to $100+ per article or project. The market is rewarding skill and specialization.

Skill-based work is more accessible. The barrier to entry for learning everything from copywriting to video editing to virtual assistance is nearly zero. Free YouTube courses exist for everything. The competition is intense, but so is the opportunity.

Social media and content creation are harder to monetize quickly but easier to grow at scale. Platforms have matured. Algorithms aren’t as friendly to new creators as they were in 2023 and 2024. But if you create good content consistently, growth still happens.

Digital products are becoming more competitive but also more profitable. Everyone knows they can create an Etsy shop now. But that means only well-designed, well-marketed products succeed. A mediocre template won’t sell. An excellent template with good marketing can earn $100 to $500 monthly.

The Opportunity:

The saturation in some areas (gig work, entry-level freelancing) actually creates opportunity for people willing to specialize and elevate quality.

Instead of doing general freelance writing, specialize in financial or health writing and charge 2 to 3 times more.

Instead of offering general virtual assistance, specialize in a specific software or type of business and charge premium rates.

Instead of applying to every gig economy platform, master one or two and become excellent.

The winners in 2026 aren’t those doing the most side hustles. They’re doing the right side hustles with excellence.

Final Thoughts: Emergency Funds as the Foundation for Everything

An emergency fund isn’t boring. It’s freedom.

It’s knowing you can handle life without fear. It’s sleeping better. It’s saying no to bad opportunities because you have options. It’s the difference between a crisis forcing you into debt and an inconvenience that you handle with savings.

I understand it’s hard to work all day and then work more on your side hustle. I understand the fatigue. I understand wanting to just relax instead of driving for DoorDash or writing freelance articles.

But I also understand the peace of mind of having three months of expenses in the bank. I understand knowing that no single unexpected event will derail your entire financial life. I understand that foundation changing everything.

Your side hustle ideas for building emergency funds aren’t about getting rich quick. They’re about getting safe. They’re about building a floor beneath your life so you can actually build up from there.

Start this week. Pick one side hustle. Commit to 15 hours. Watch your first paycheck hit your emergency fund. Feel how good that feels. Then do it again next week.

Twelve months from now, you’ll have an emergency fund. Twelve months after that, you’ll have options. That’s how this works.

My strongest salute goes to everyone starting their side hustle journey right now. You’re not chasing quick money. You’re building real security. That’s courageous work. That’s important work. And it absolutely matters.

Disclaimer: This article is for educational and informational purposes only. It is not financial, investment, or legal advice. Always consult a qualified financial advisor before making any financial decisions.

Richard Patterson is the founder of Payoff Hustle. With over 8 years of experience in personal finance and online income, he has helped thousands of people build profitable side hustles while working full-time jobs.

4 thoughts on “10 Side Hustle Ideas for Building Emergency Funds That Actually Work in 2026”